Back on March 11th of this year I wrote a Weekend Report called, Gold’s Confirmed Breakout. I posted mostly some long term charts we’ve been following during the 4 1/2 year consolidation phase which is finally coming to fruition. They say patience is a virtue, but 4 1/2 years is a long time to be patient.

Preservation of capital in such a large trading range can be quite difficult for many investors as they either lose interest or become despondent that nothing positive is taking place and try to make trades where there are none. We did make a few trades during that 4 1/2 year trading range mostly breaking even, winning a few and losing a few which is the nature of a range bound market. Luckily we were trading the long side of the US stock markets which helped time pass.

Tonight I’m going to update what I wrote in the Weekend Report on March 11th so you can see what we were looking at to be able to call the low within just a few days. We bought our first Kamikaze stock on March 4th and with most of our PM stocks on March 5th. That small false breakout which turned into a bear trap was one of our many clues.

I’m going to show you what I wrote in the March Weekend Report with the chart and then we’ll look at the updated chart as of this past Friday.

March 11th 2024:

Weekend Report…Gold’s Confirmed Breakout

I know the title of this Weekend Report may sound a little bold, but after tracking the 2020 trading range from every imaginable point of view I can say with a strong vote of confidence that the beginning of the next important advance in its secular bull market for Gold, that began at the 2000 low, is underway.

We could still see a backtest to the breakout point, but that would just be part of the breaking out and backtesting process.

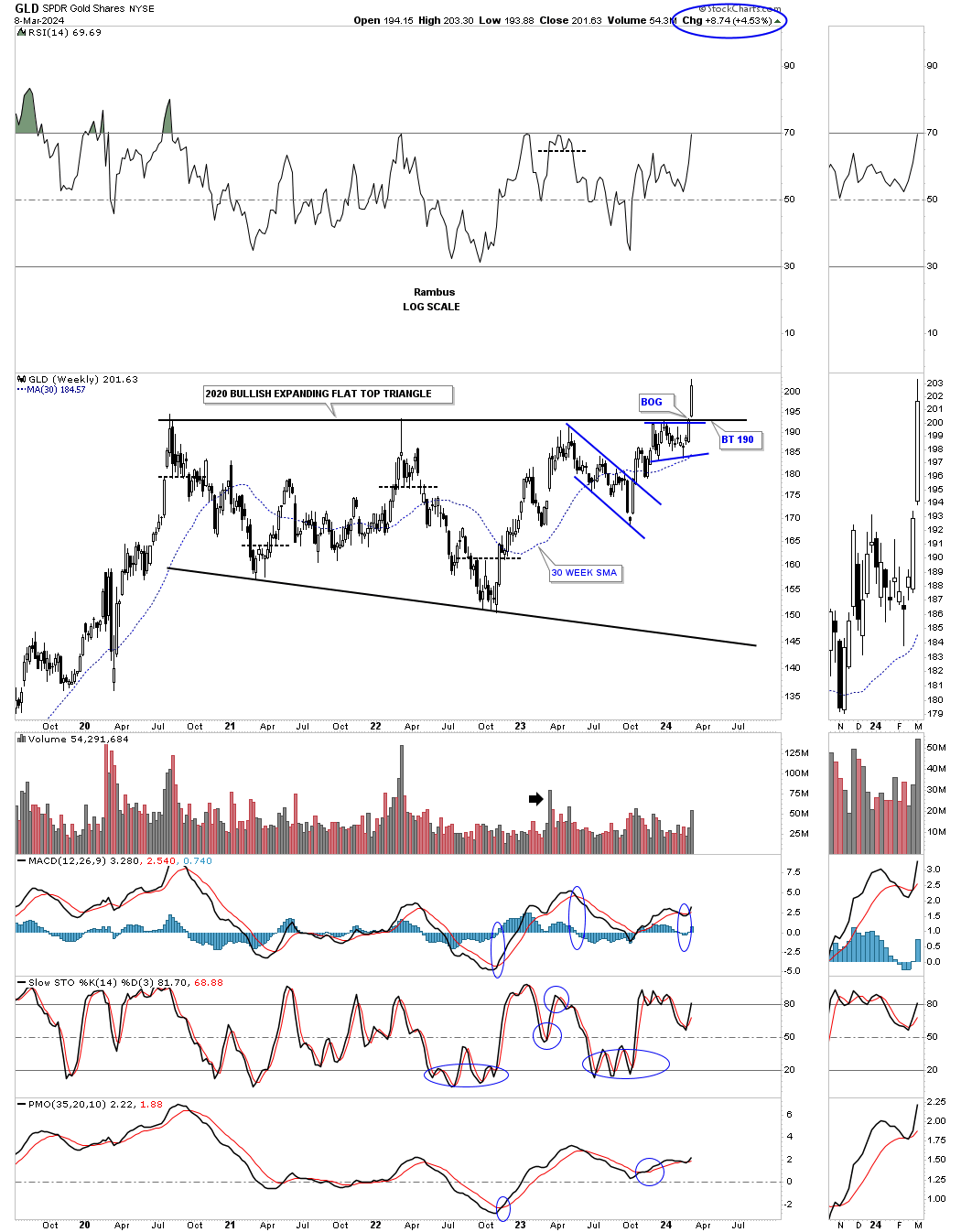

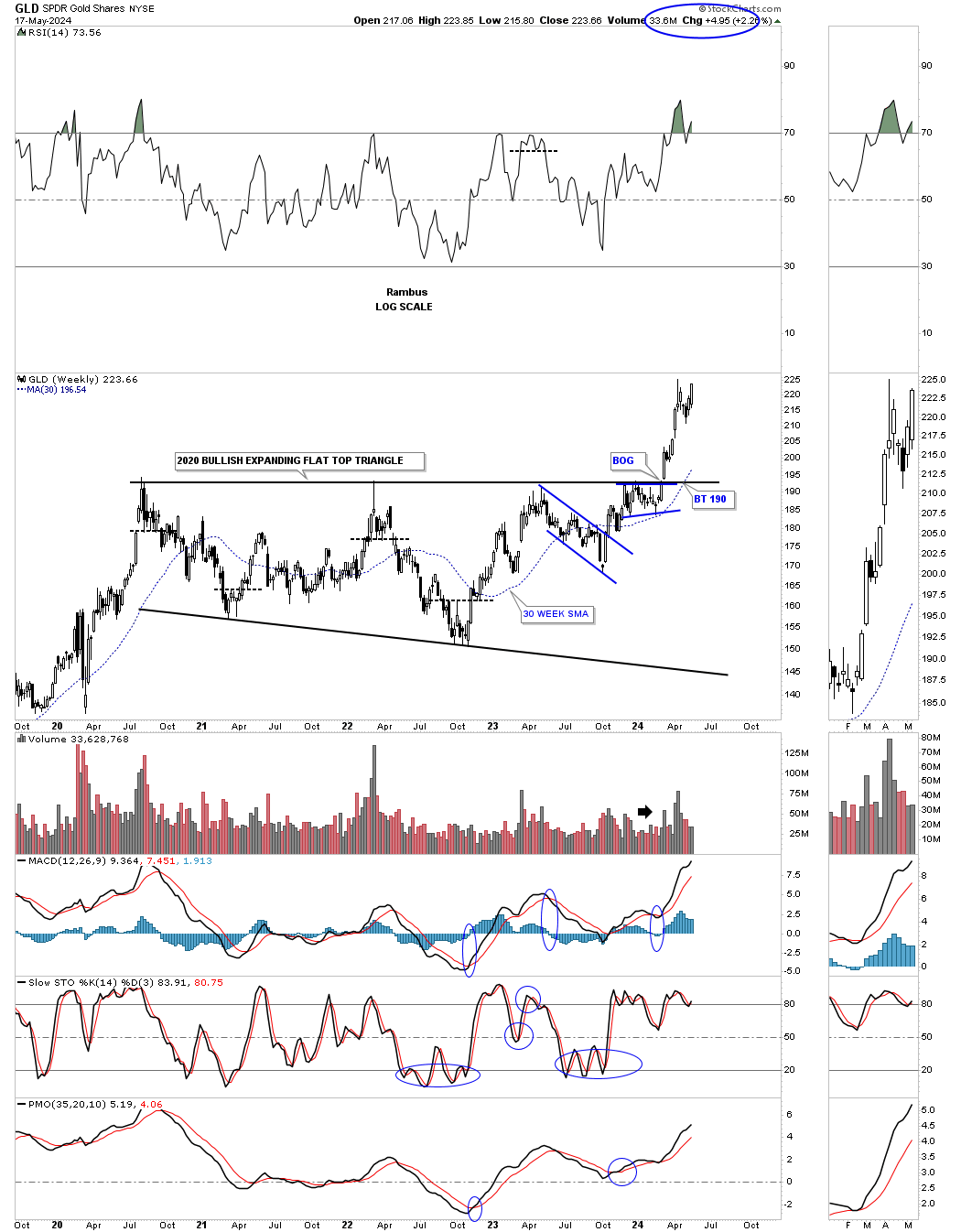

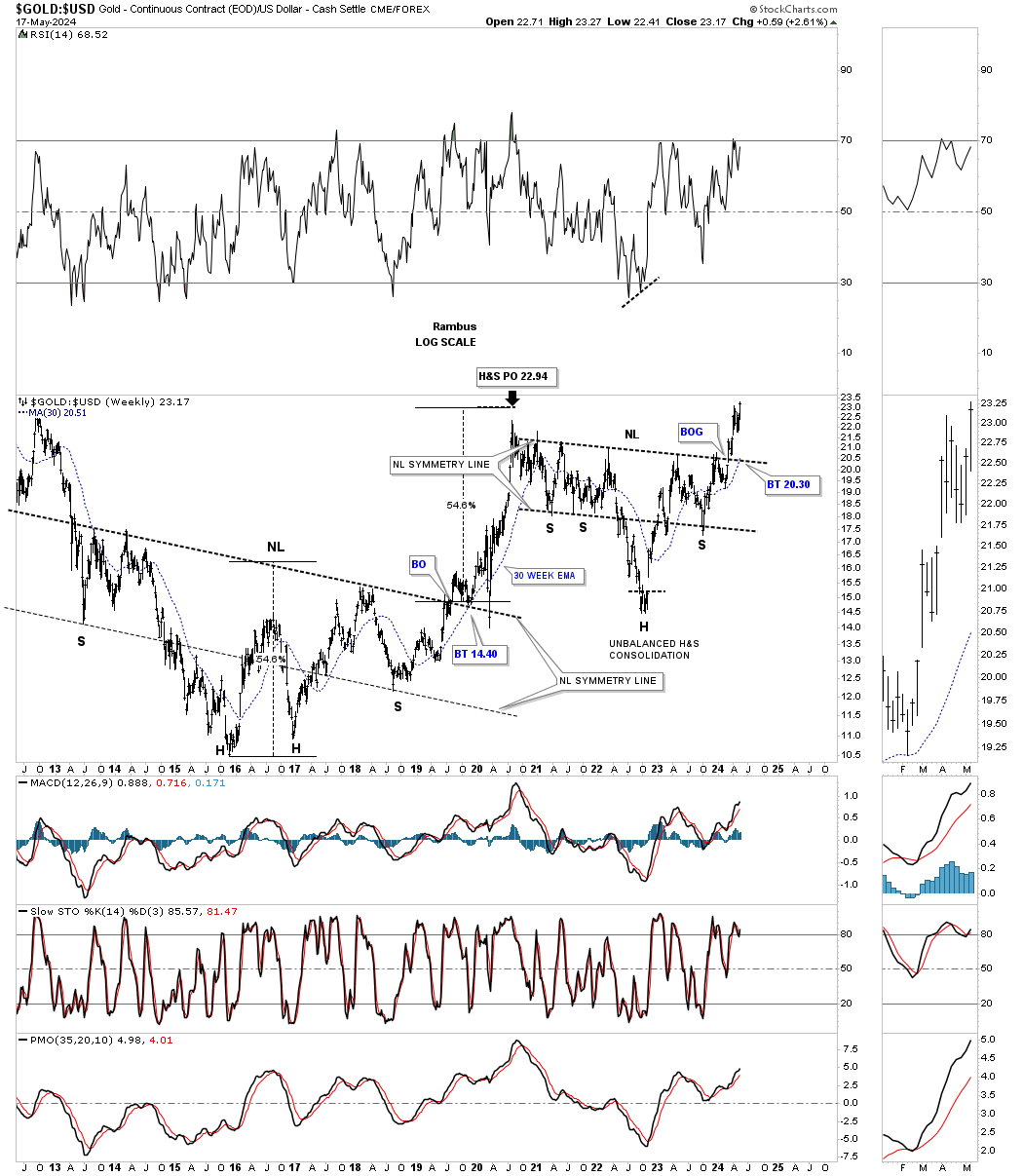

Lets start with the weekly chart for the GLD which shows the 2020 trading range which I’ve labeled as a flat top expanding triangle. This nearly 4 1/2 year consolidation pattern can also be called a cup and handle or a H&S consolidation. At this point it’s just semantics.

Last Monday March 4th you can see the breakout from the 2020 bullish flat top expanding falling wedge. Its a bit hard to see on this long term weekly chart, but if you look at the thumbnail on the right sidebar you can see the breakout gap that occurs on Monday. The top trendline of the 2020 trading range has always been tough to figure out exactly where to draw it, you know one was there, but there were several different ways it could have been drawn. With the breakout gap last Monday there is no doubt on how the top rail can now be applied.

Today May 19, 2024:

This is the updated chart as of Friday. The breakout gap never got backtested which also happened during the breakout from that massive 2016 H&S consolidation pattern we watched build out which felt like an eternity also before the breakout.

March 11, 2024:

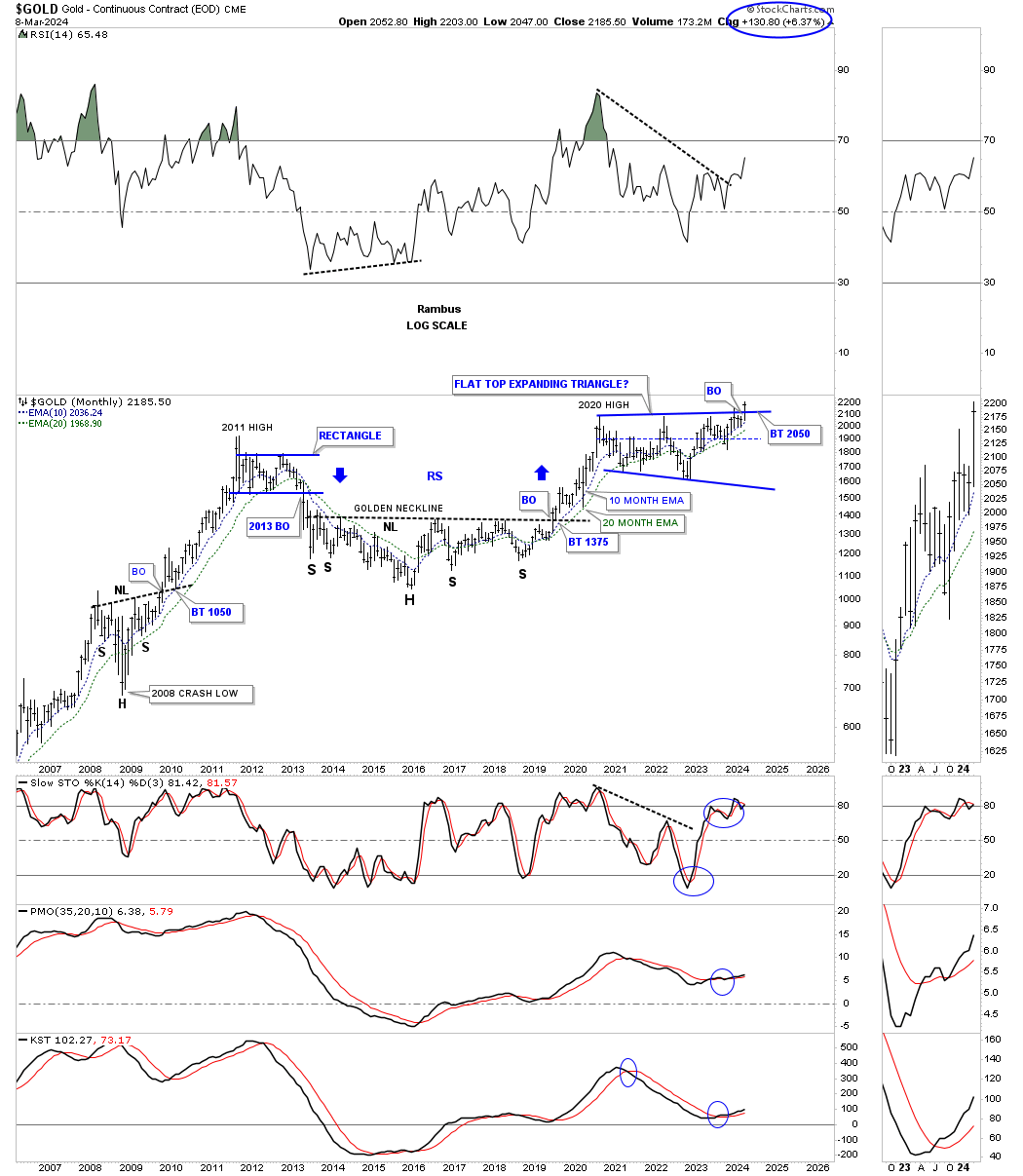

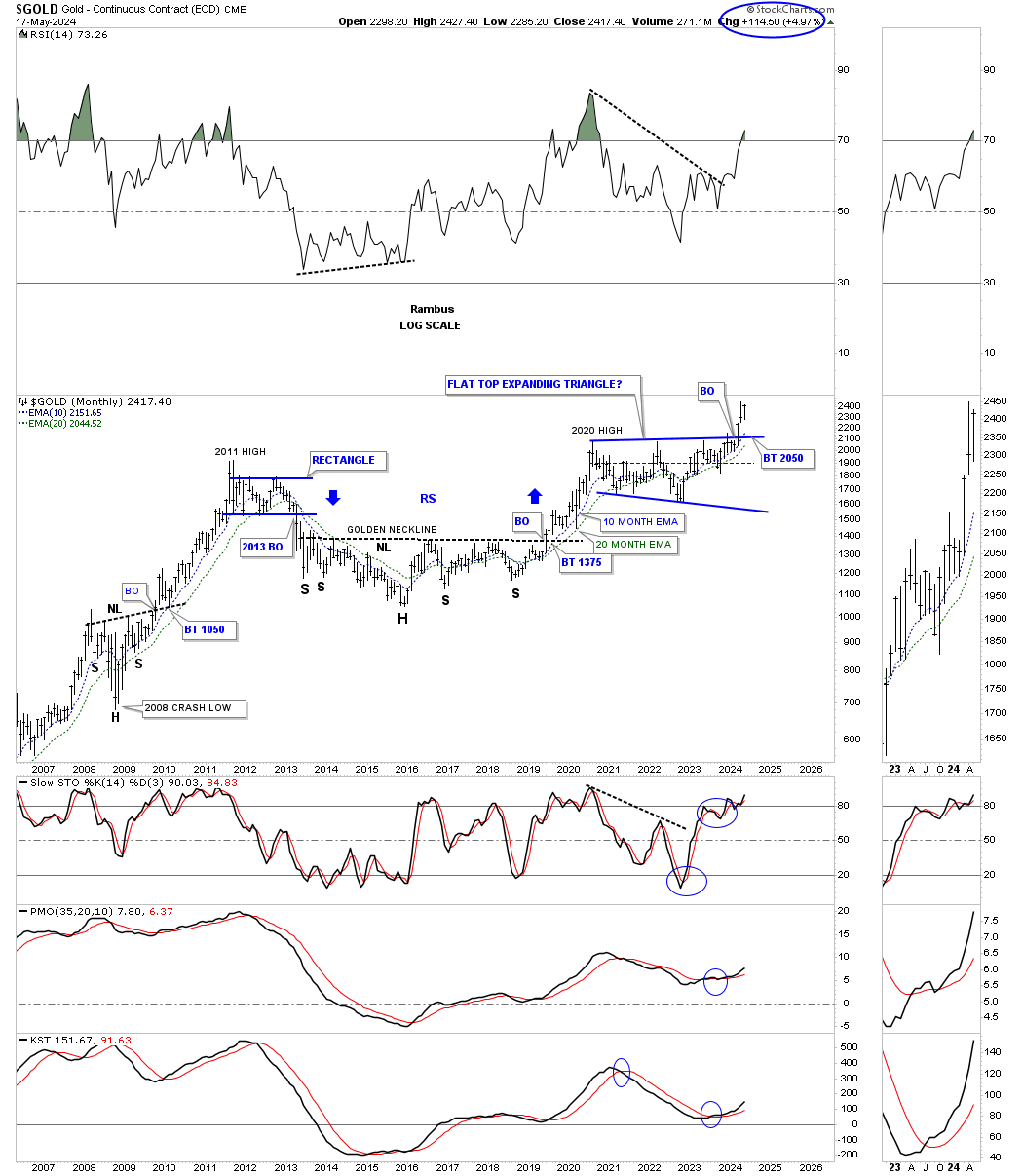

Next is a longer term monthly chart which puts the 2020 trading range into perspective. This chart starts at the 2008 crash low where Gold formed a beautiful H&S consolidation pattern which launched Gold on its way to the 2011 all time high.

Next came the bear market which bottom in 2016 which created the head of the very large 2016 H&S consolidation pattern. The breakout from the 2016 H&S consolidation pattern led to the next important impulse move which topped out just above the 2011 high in 2020.

Keep in mind the job of a consolidation pattern is to sow doubt in your mind about the validity of the bull market and after 4 1/2 years few will have a hard time adjusting to the new paradyme shift that is now taking place from consolidation to impulse. Also the bigger the consolidation pattern the bigger the impulse move.

Today May 19, 2024:

The new impulse move continues.

March 11, 2024:

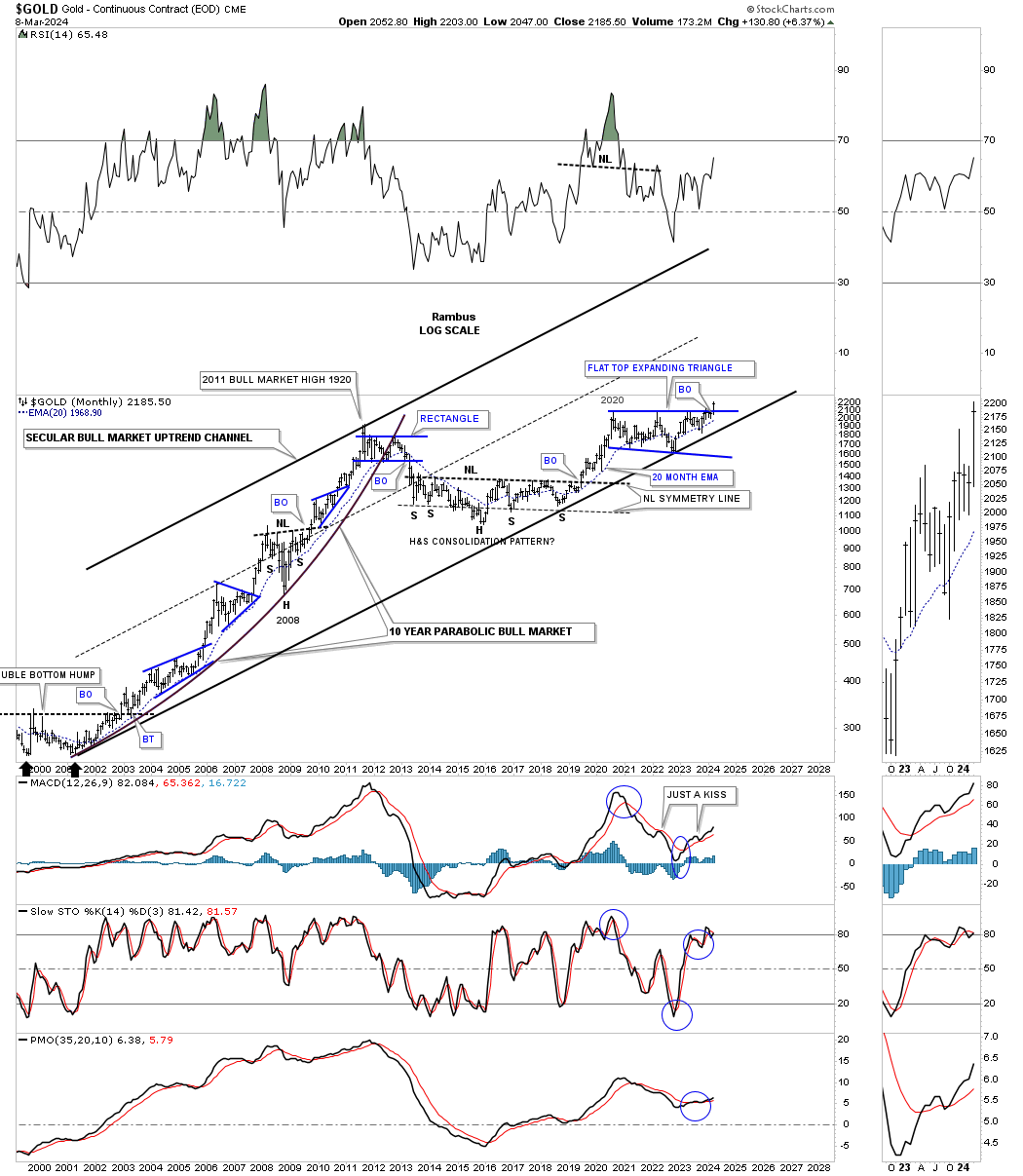

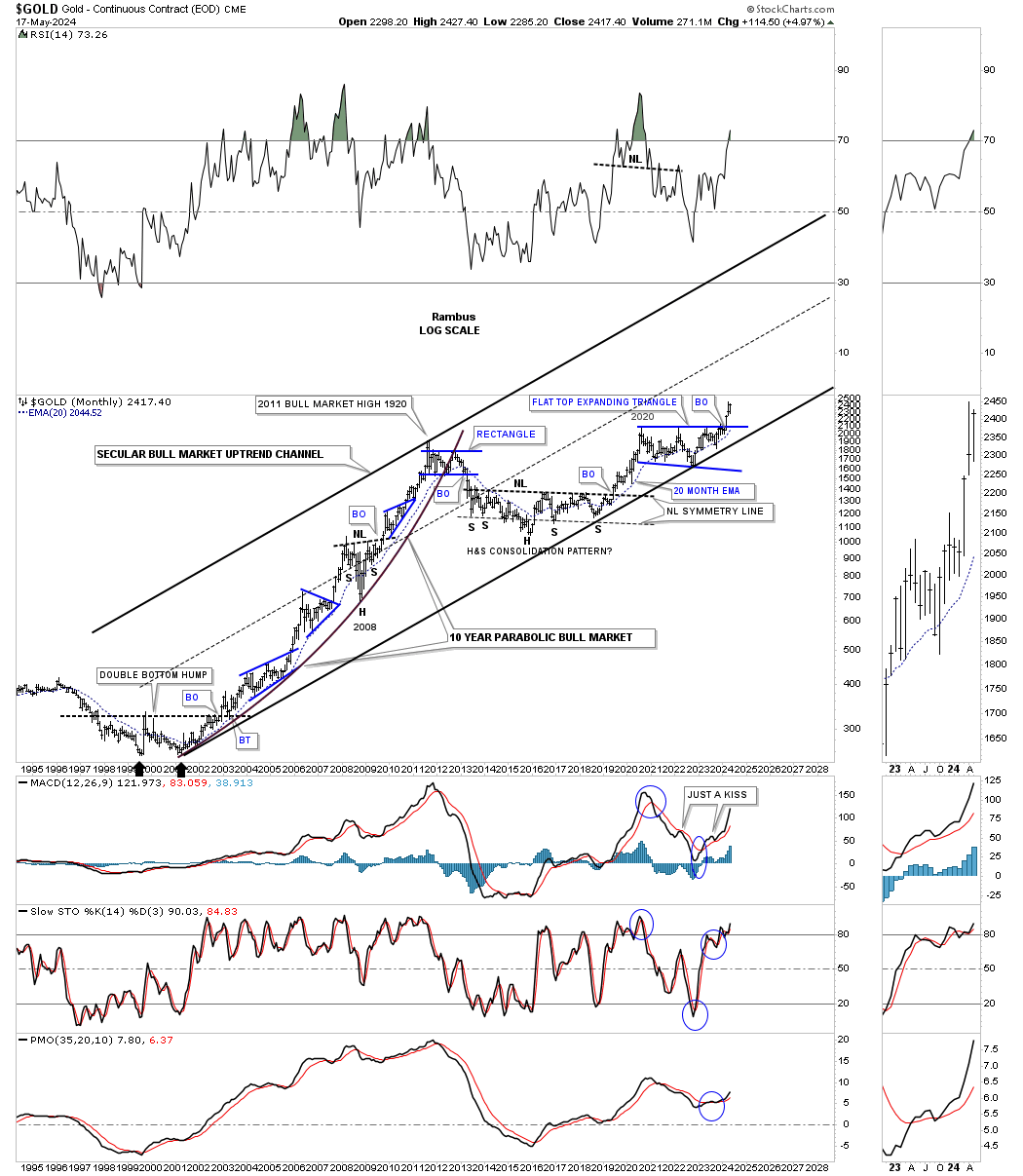

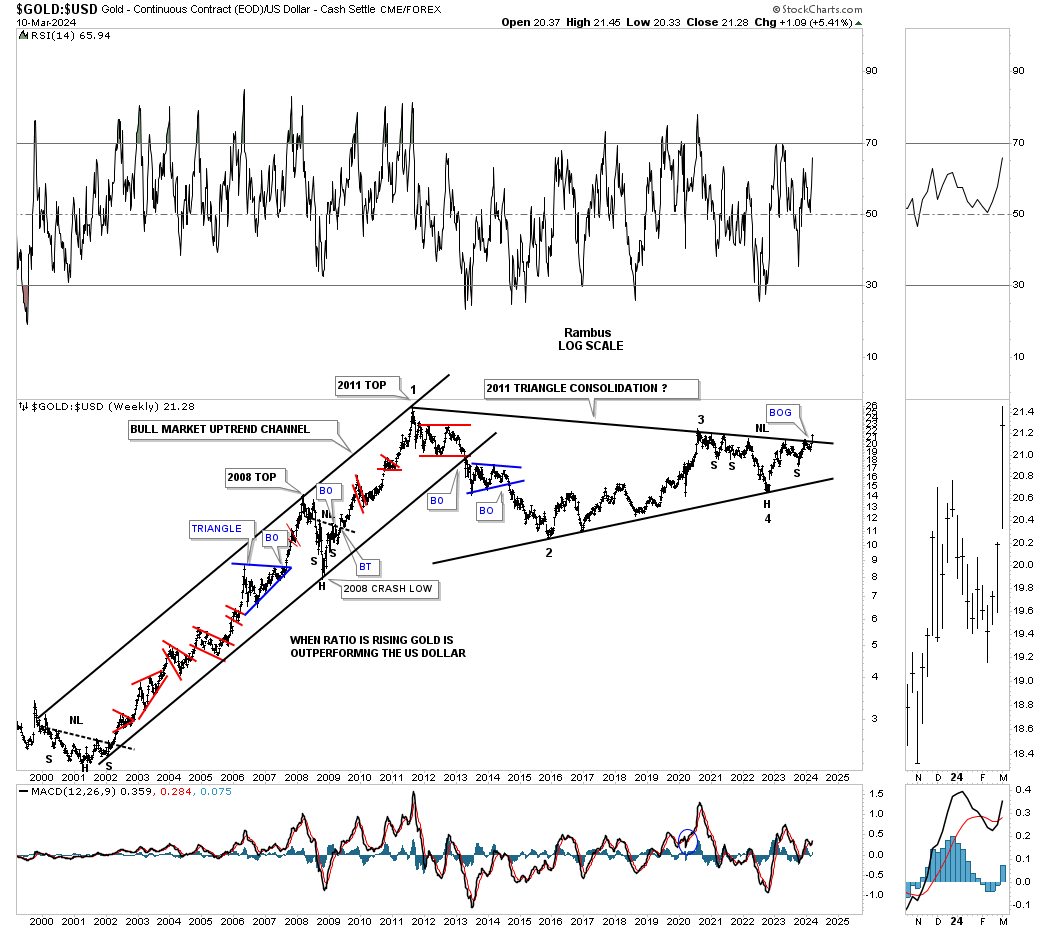

In Friday’s Market Update I mentioned how the QQQ has overtaken the beautiful Chartology of the bull market consolidation patterns that Gold had made during its 2000 to 2011 bull market run with one consolidation pattern forming on top of the previous one as shown on the chart below. Even on this log scale chart you can see the bull market was going parabolic into the 2011 high.

As you can see the bottom trendline of the 2000 secular bull market uptrend channel has been tested on several occasions with the last one being the October 2022 low. Now we can see the monthly bar all by itself above the top rail of the 2020 trading range. Also note how well the 20 month ema has held support during strong advances.

May 19, 2024:

We can now add two more monthly bars on this breakout move.

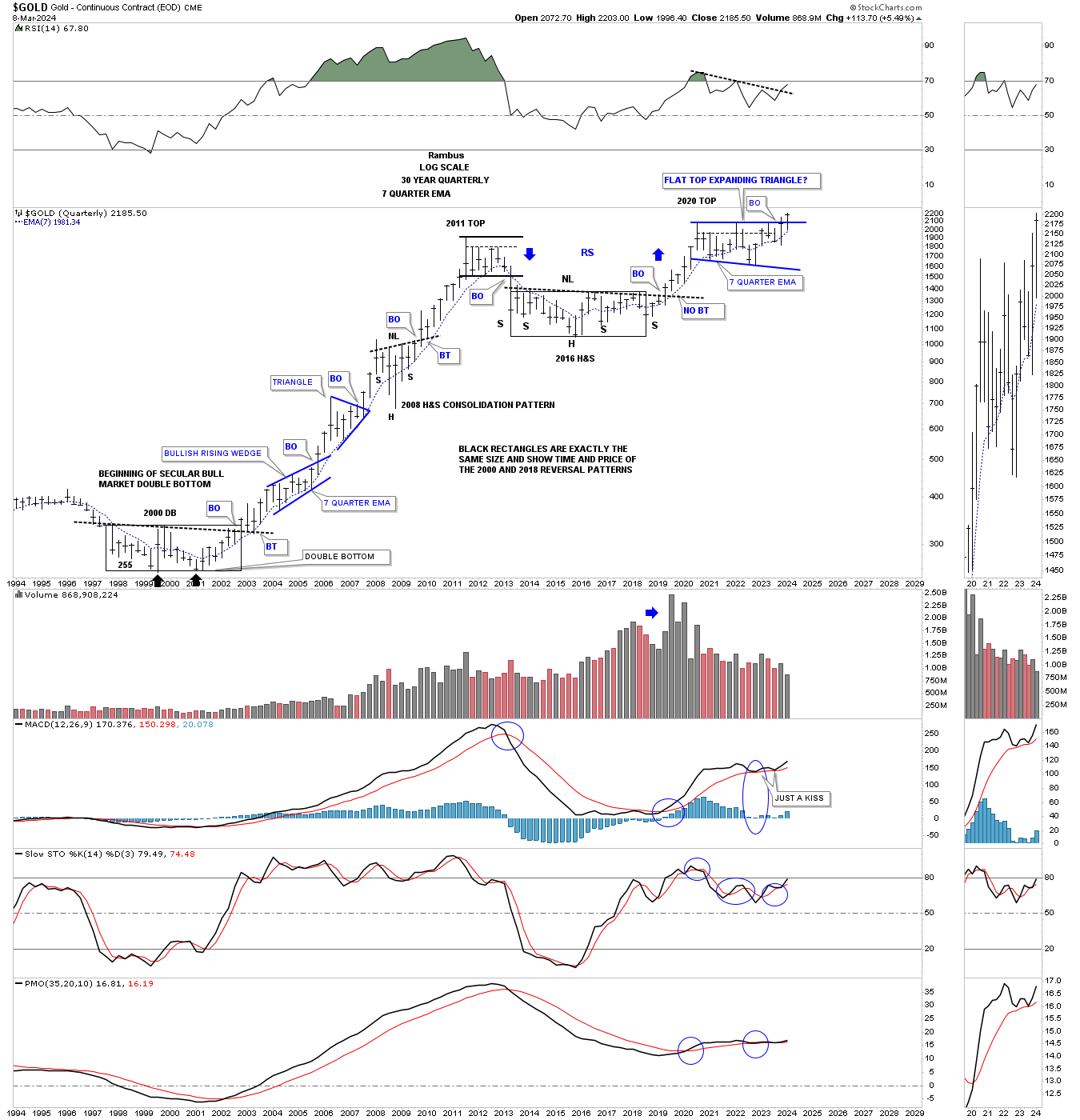

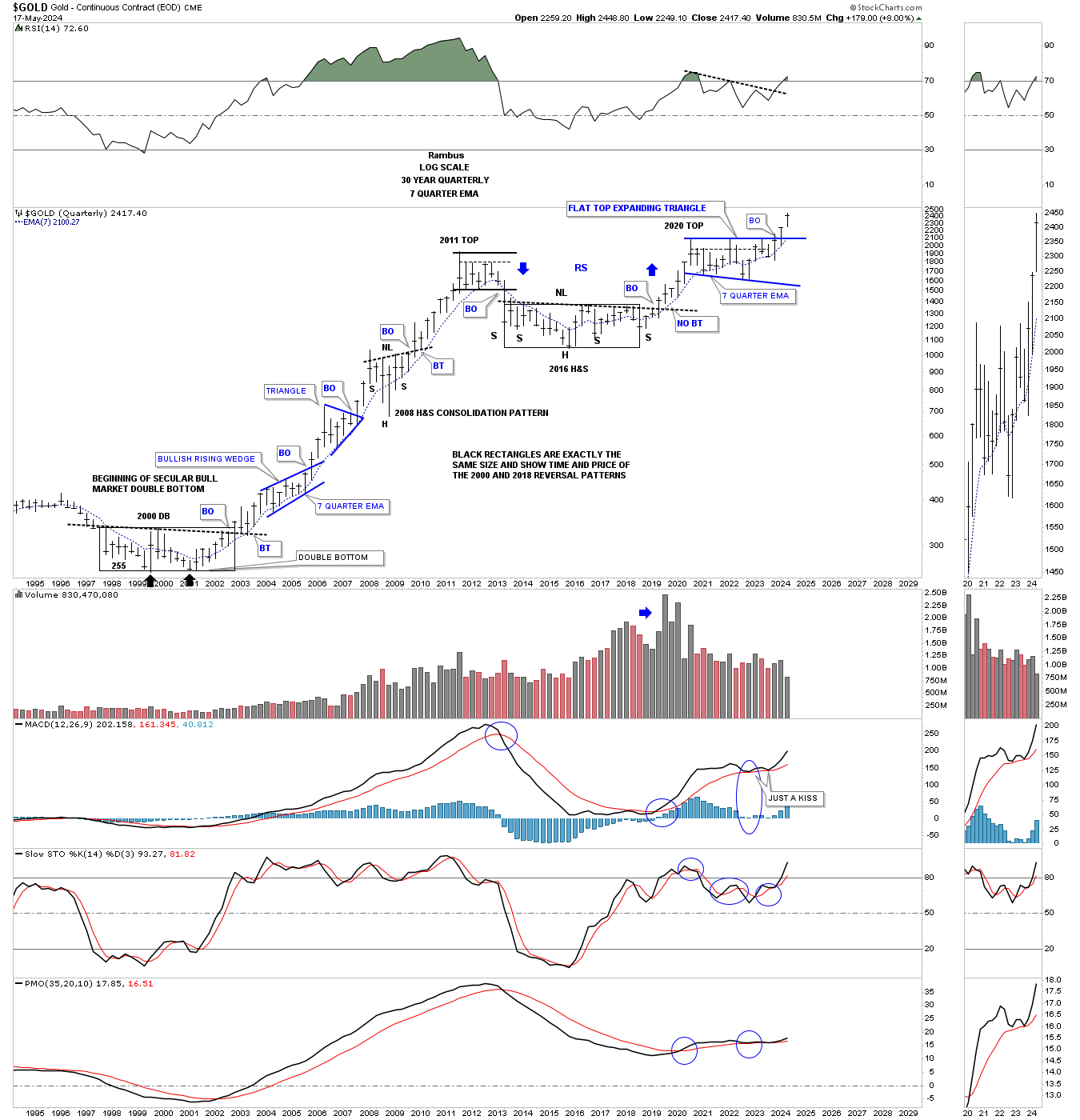

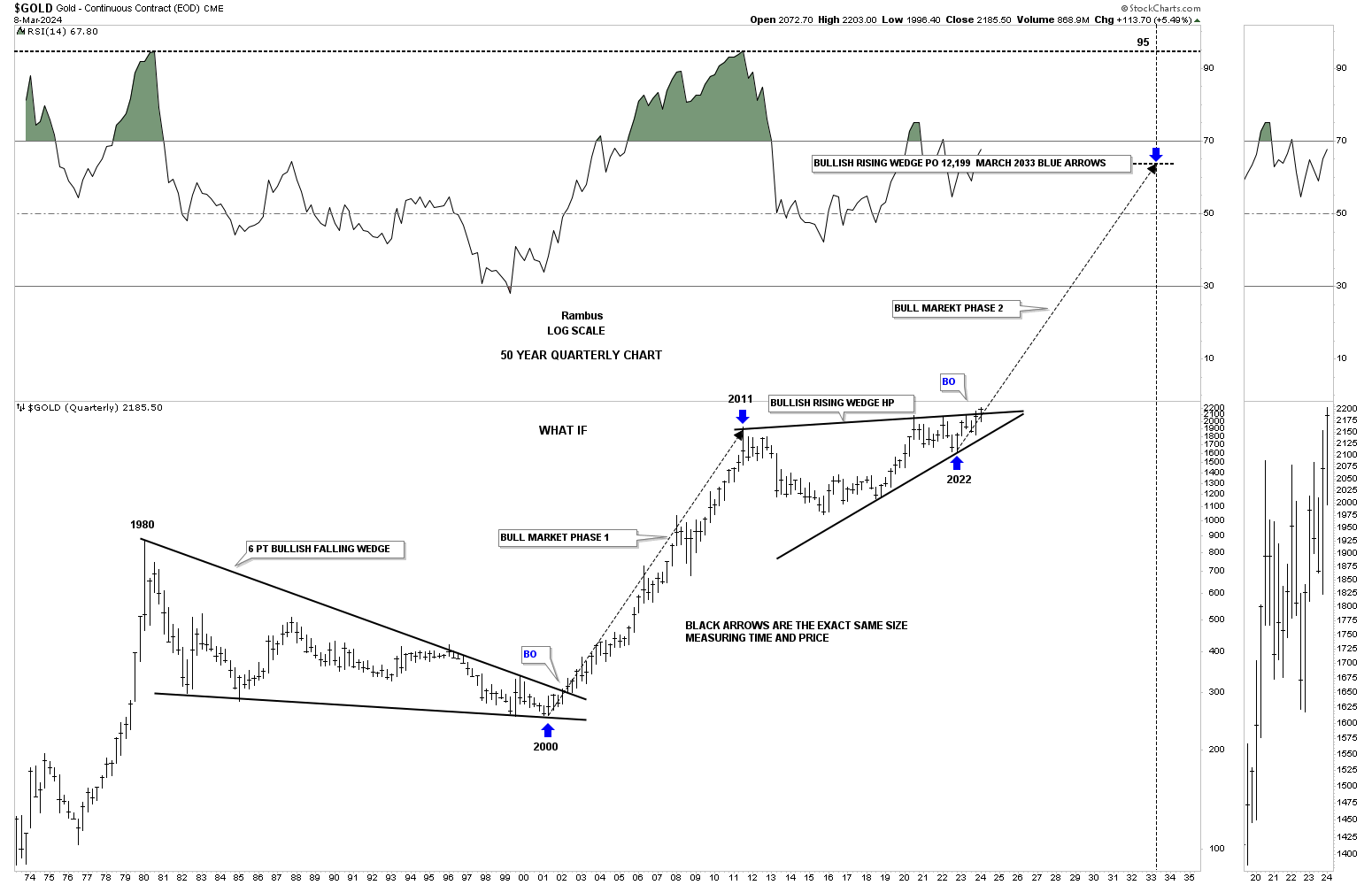

March 11, 2024:

This 50 year quarterly chart compares the 2000 base to the 2016 base with both rectangles being exactly the same size measuring time and price. If the 2000 base was large enough to launch an eleven year bull market it would make sense that the 2016 base should be big enough to launch a similar bull market.

The first consolidation pattern that formed when Gold broke out of the 2000 double bottom base was the blue bullish rising wedge. The first consolidation pattern to have formed since the breakout from the 2016 base is the 2020 blue flat top expanding triangle. Note the impulse moves when a consolidation or reversal pattern is complete.

May 19, 2024:

How long will this 2nd quarterly bar look when the 2nd quarter comes to an end in the next six weeks?

March 11, 2024?

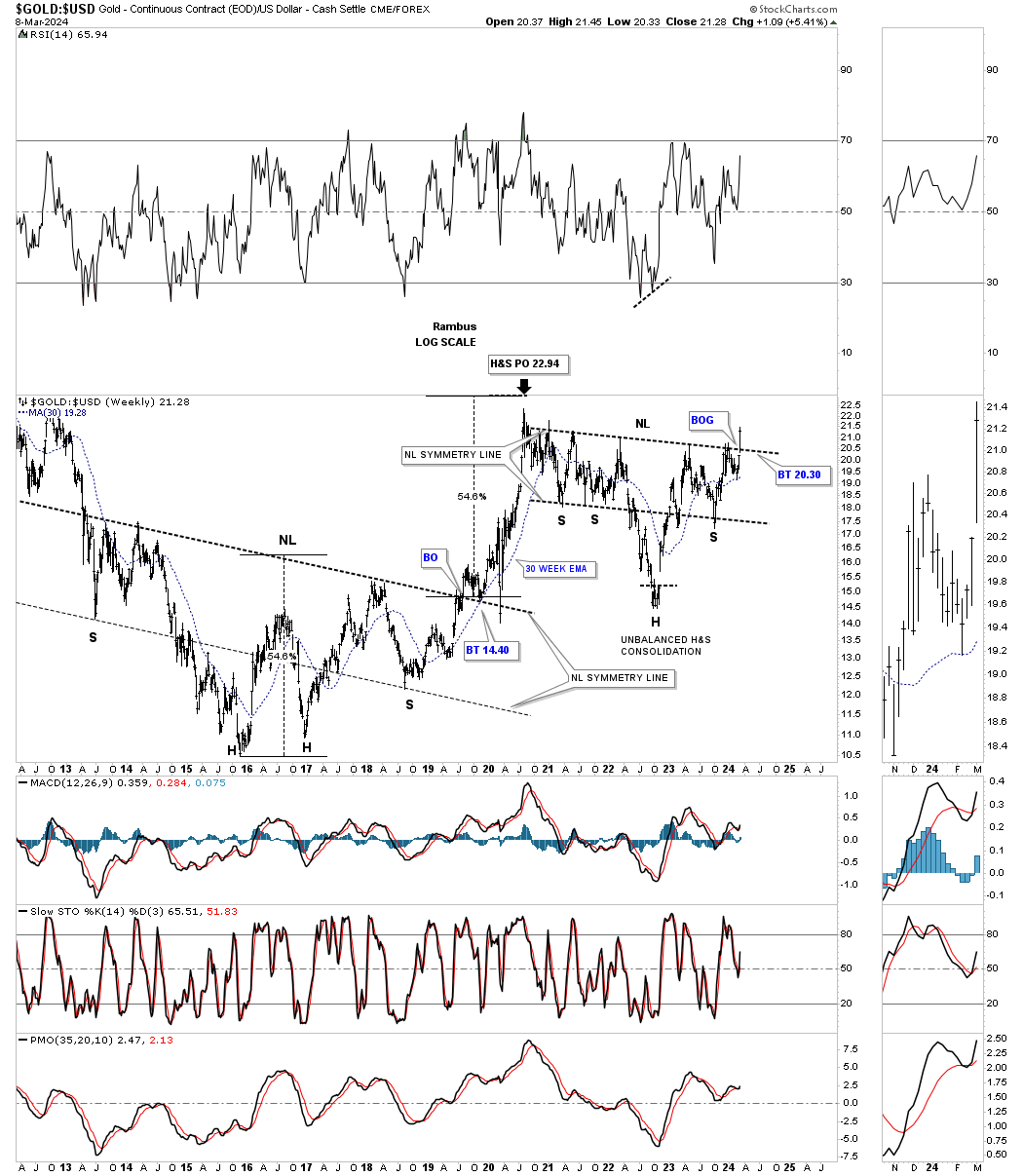

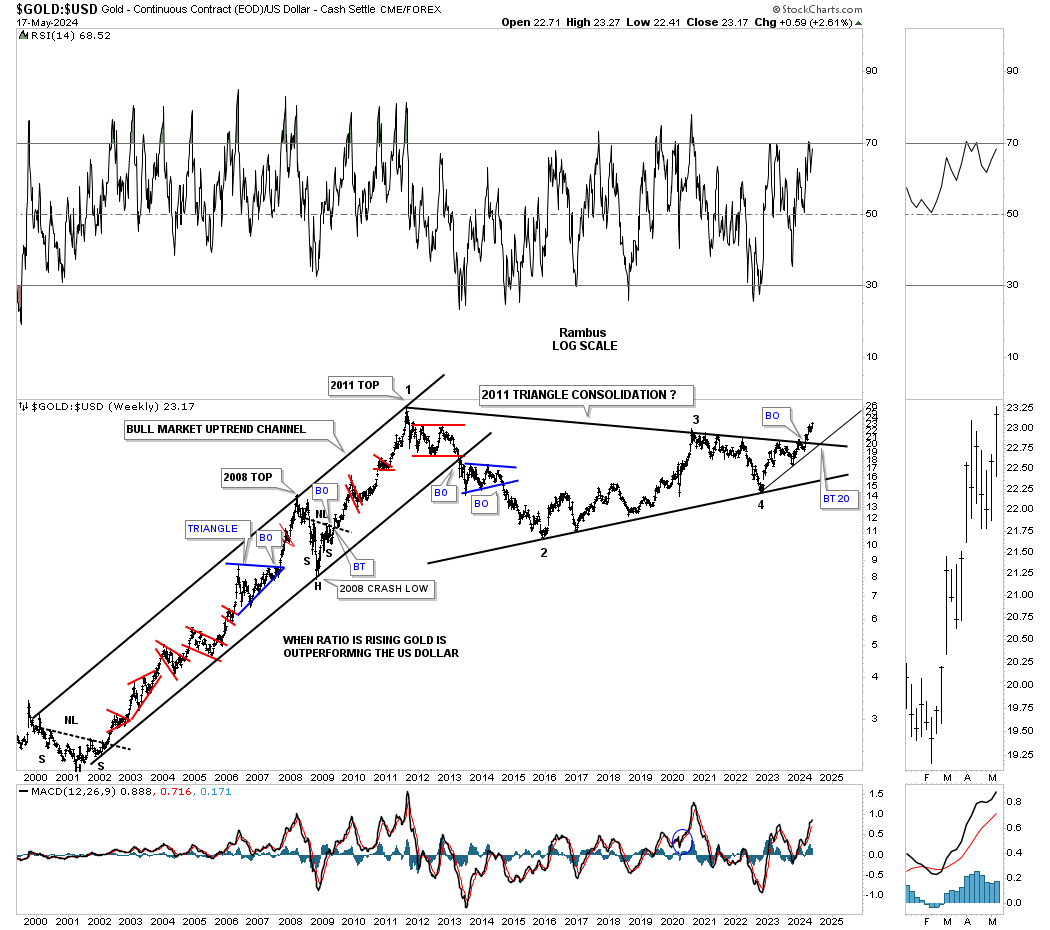

Another big clue that the 2020 correction is over for Gold is this ratio chart which compares Gold:US dollar. Note the very large H&S bottom that formed when Gold was building out its own 2016 H&S base. The neckline symmetry line showed us the low for the right shoulder. You can also see how close the price objective was to the actual high that was made at the 2022 high. Again, last Monday you can see a breakout gap above the neckline of the unbalanced H&S consolidation pattern, see thumbnail on right sidebar of the chart for a better view. We need to see Gold outperforming the US dollar, the stronger the better.

May 19, 2024:

The backtest to the neckline held support with a new higher high this week.

March 11, 2024:

Lets take the Gold:USD ratio a step further and go all the way back to the 2000 low. As you can see Gold outperformed the US dollar for eleven years with only small consolidation patterns forming along the way.

Once again look at the thumbnail on the right sidebar which shows the breakout gap from last Mondays breakout move above the 2011 triangle consolidation pattern. We’ve literally been following this massive triangle for several years and to finally see it come to fruition it’s pretty rewarding. Big patterns lead to big moves.

Note the H&S consolidation pattern on the chart above. You can see how it fits into the apex of the 2011 triangle which was strongly suggesting the top trendline was going to give way.

May 19, 2024:

The breakout gap from the massive 2011 triangle was never backtested with Gold making a new higher high against the US dollar this week.

March 11, 2024:

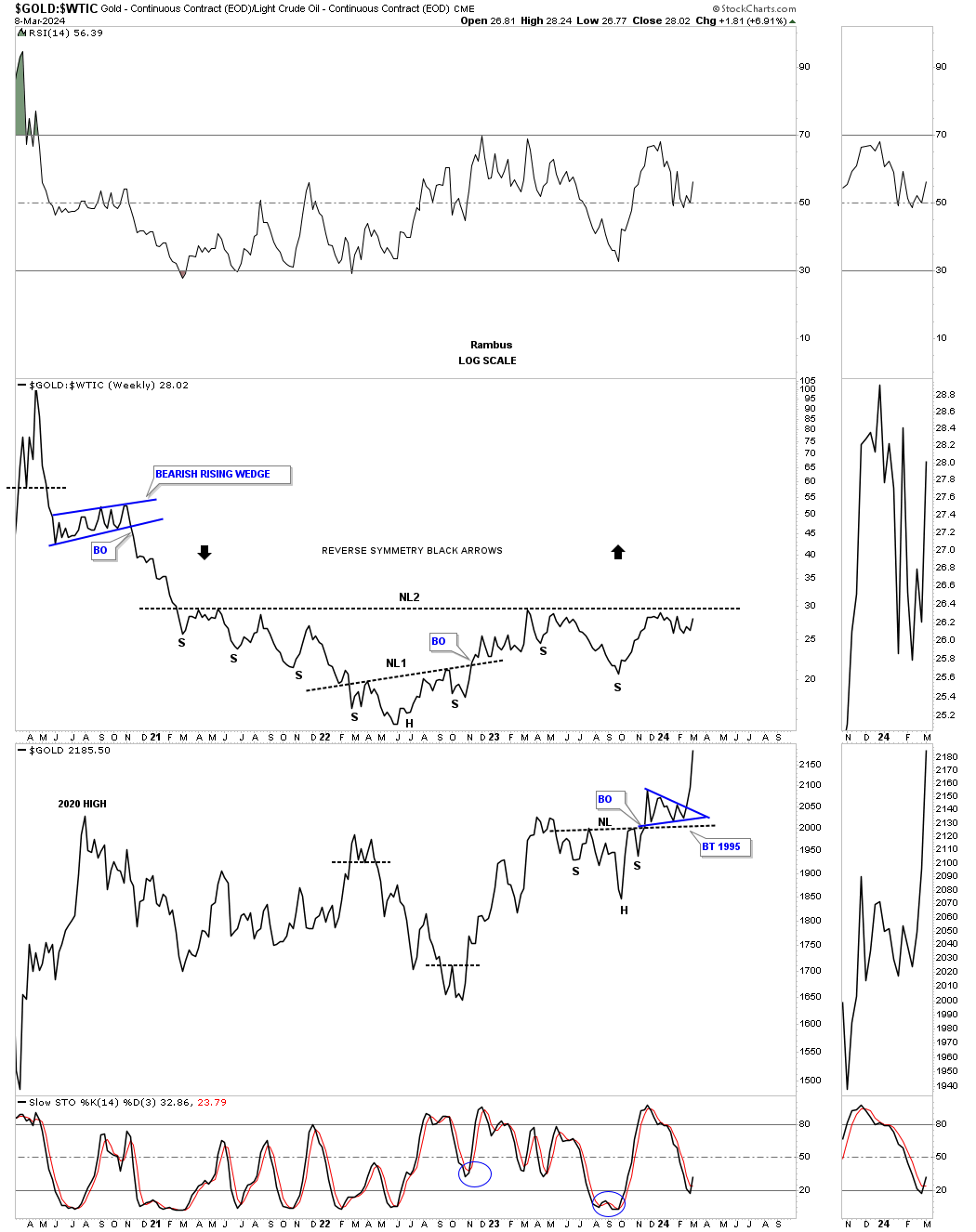

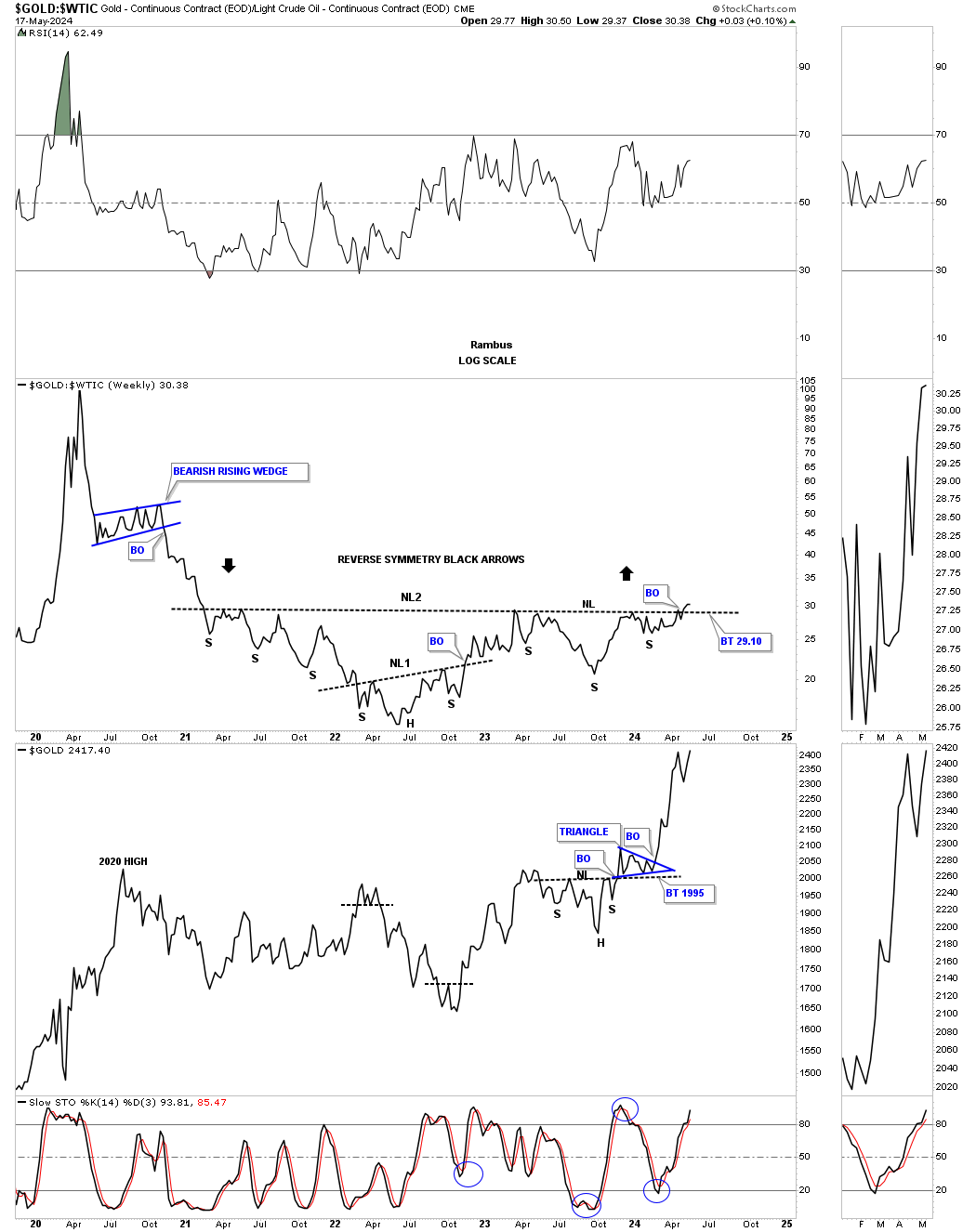

Below is a ratio combo combo chart with the Gold:WTIC on top with Gold on the bottom. There is still a bit of work to do on the ratio chart, but if the neckline is taken out to the upside that should be a good tailwind for the entire PM complex.

May 19, 2024:

We now have the breakout.

March 11, 2024:

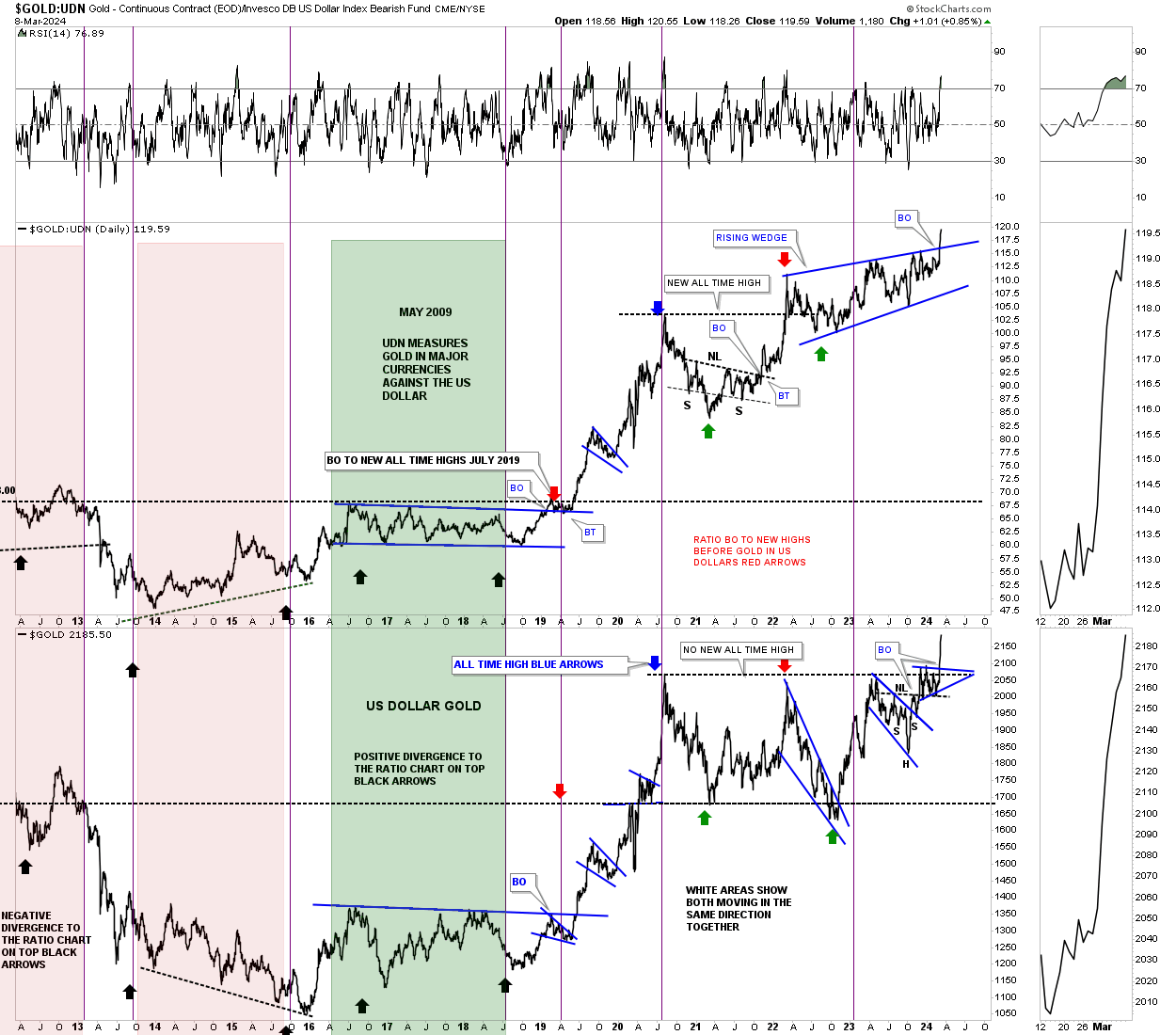

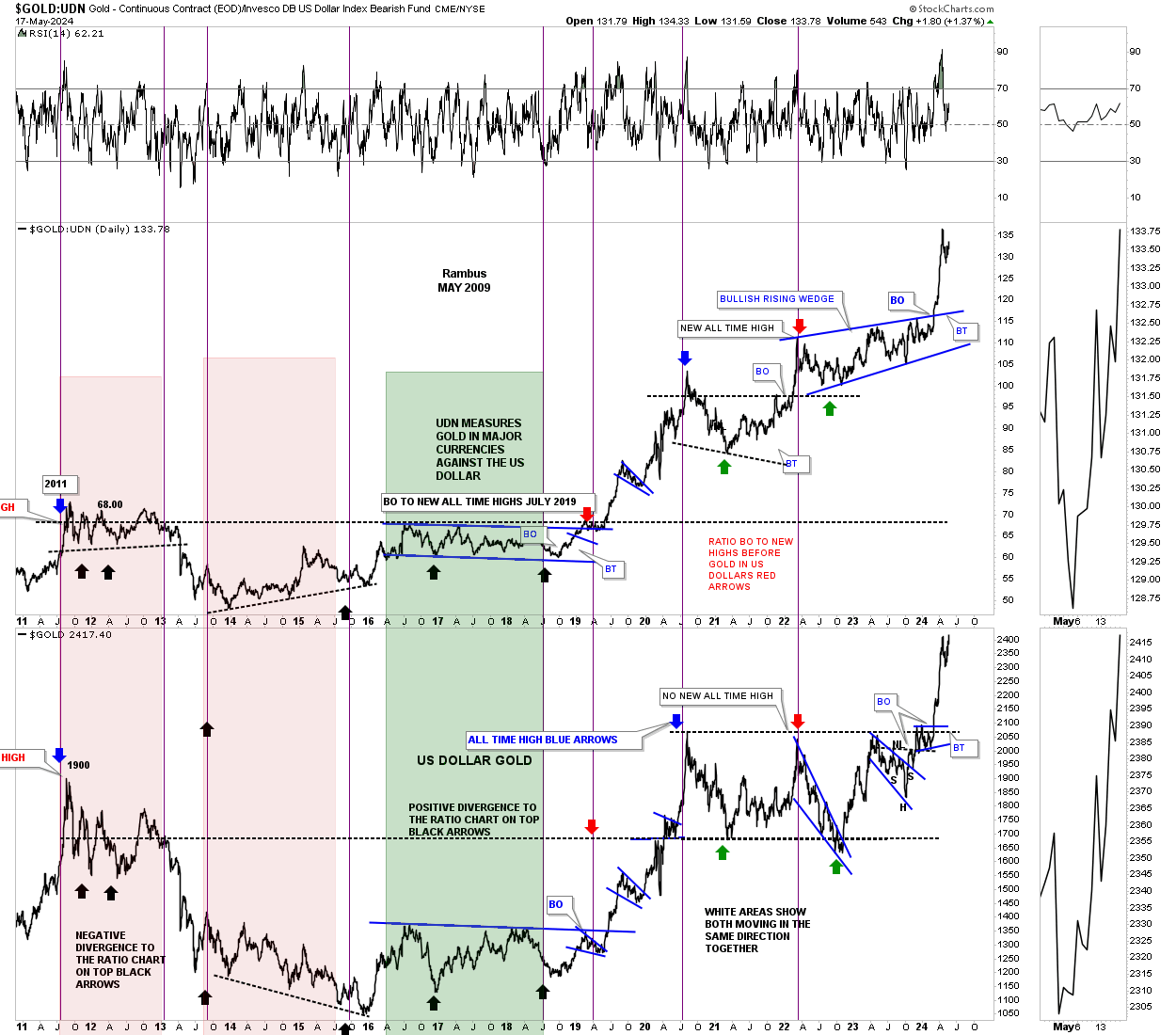

Another major clue took place last week on this ratio combo chart which compares Gold:UDN ratio on top with Gold on the bottom. The Gold:UDN ratio shows how Gold is performing in many of the important currencies of the world ex the US dollar. As you can see the 2022 blue bullish rising wedge broke out into new all time high territory. It doesn’t happen all the time, but Gold in US dollars on the bottom chart also broke out into new all time high territory. Your best rallies in Gold come when both are moving up together.

May 19, 2024:

Both have had a strong impulse move so far.

March 11, 2024:

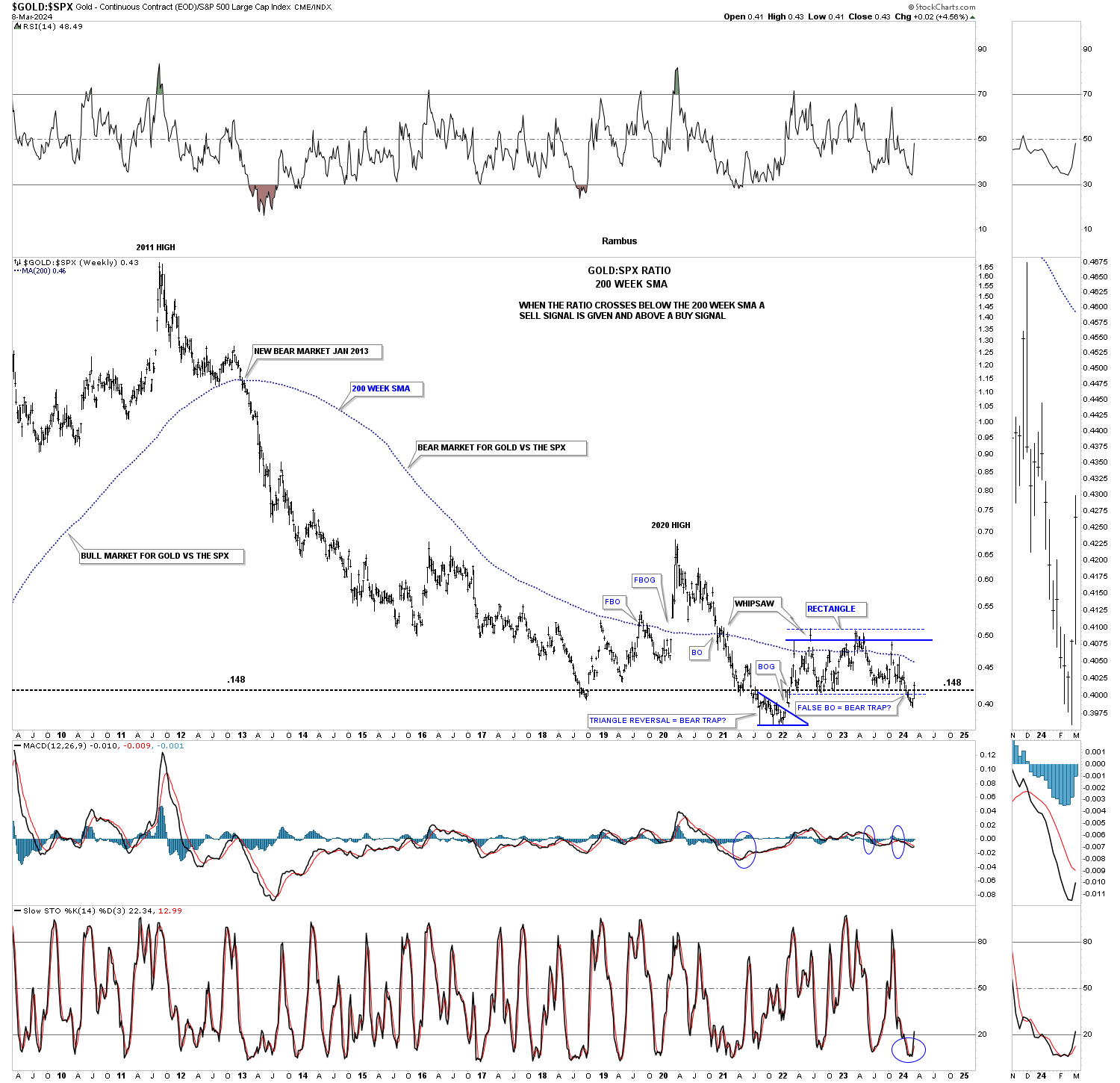

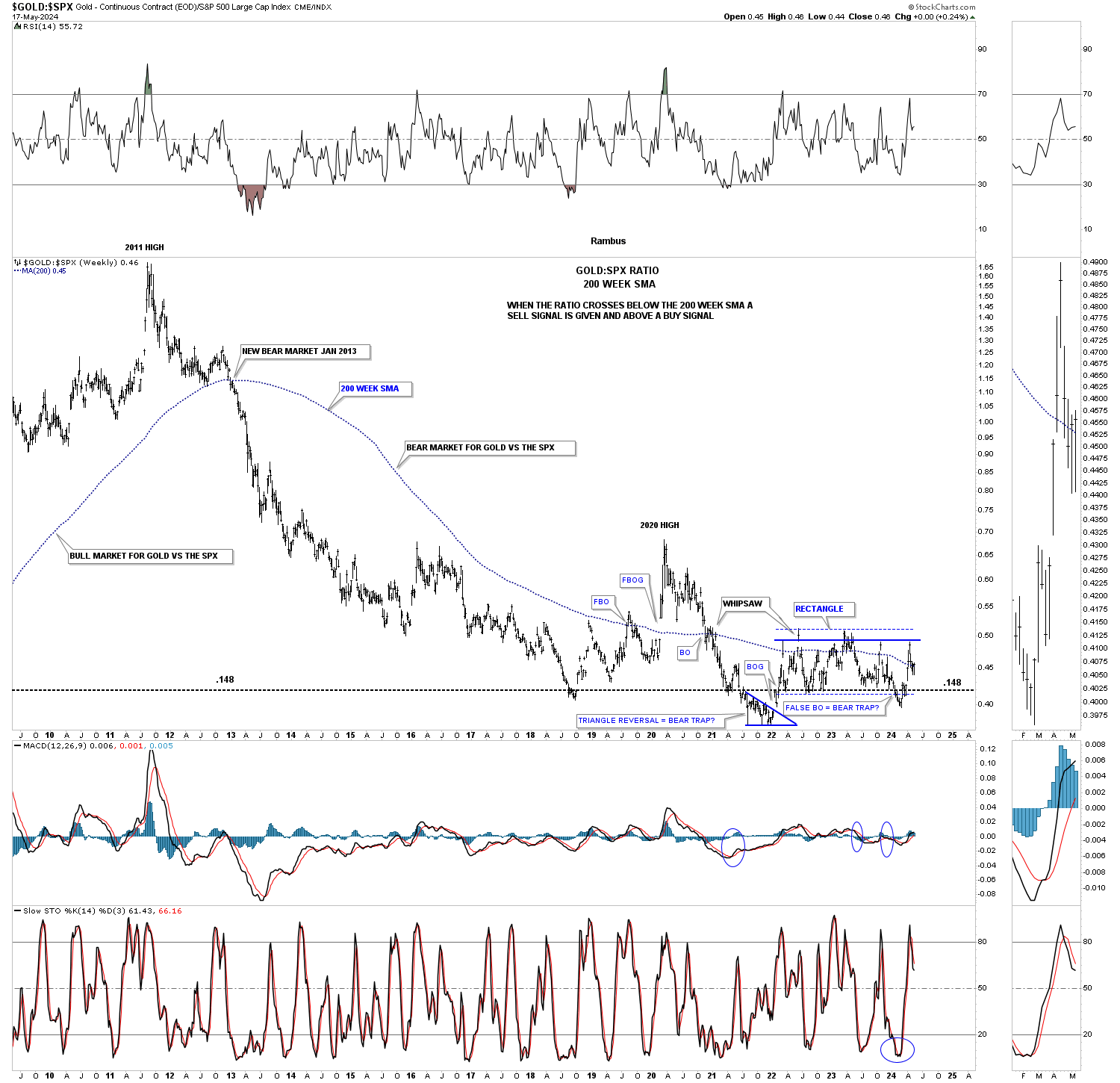

Gold can have its strongest rallies when it’s outperforming the SPX. Since the 2011 high you can see, compared to the SPX, Gold has been declining even though it is at record highs. There could be a possible bright spot at the bottom of the chart where the ratio may have completed a false breakout below the blue rectangle which could now setup as a bear trap. Since the ratio is trading back inside of the blue rectangle the breakout is negated for now.

May 19, 2024:

The ratio made it back up to the top rail of the blue rectangle. It would be a very bullish sign for the PM complex in general if we see the top rail of the blue rectangle taken out meaning Gold is outperforming the SPX. We also need to see the ratio trade and stay above the 200 week sma to really outperform the SPX in a new bull market.

March 11, 2024:

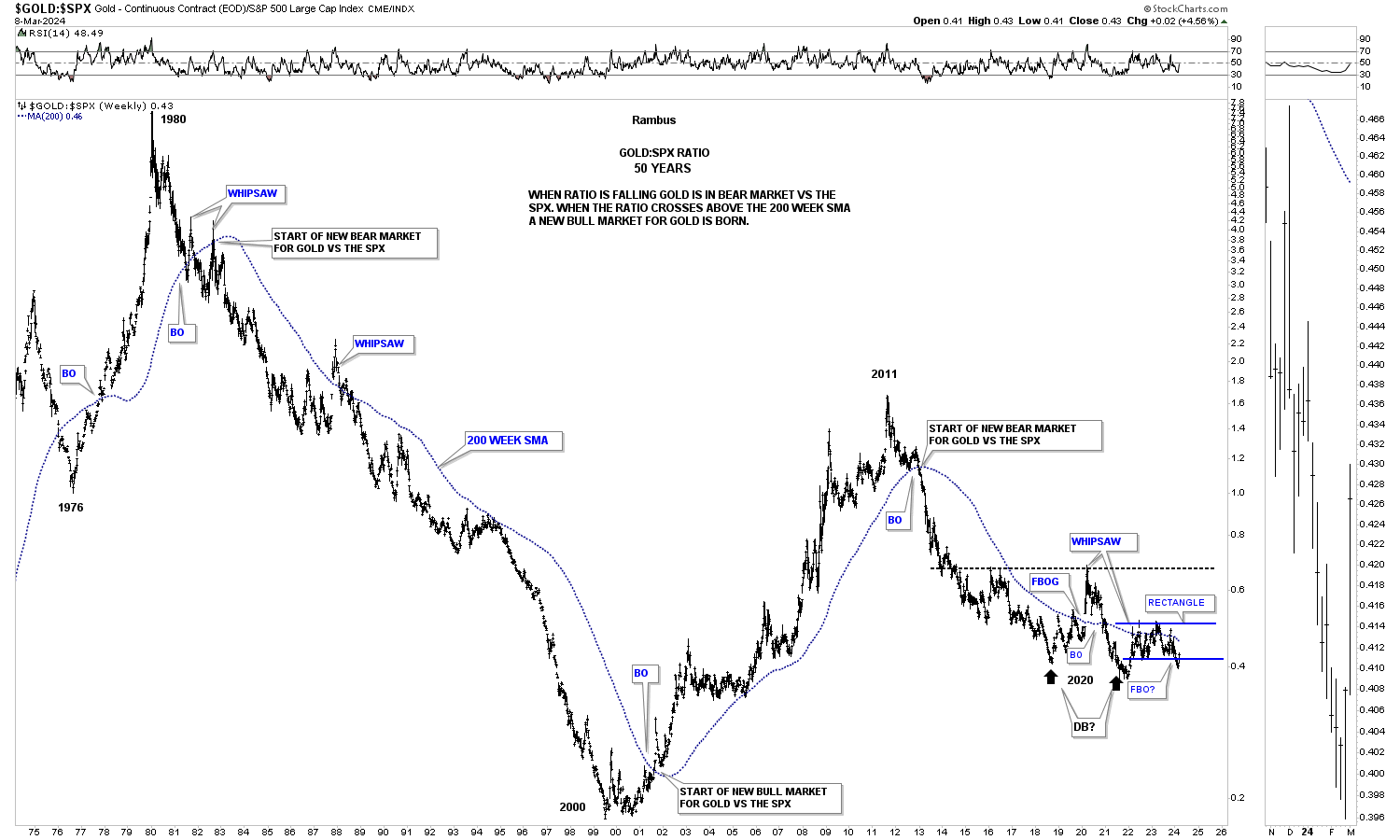

Below is a much longer term 50 year chart for the Gold:SPX ratio using the 200 week sma. The 200 week sma does a very good job of keeping you on the right side of the trend. When the ratio is falling the SPX is outperforming Gold and vise versa in the other direction. There is an occasional whipsaw, but the 200 week sma lets you know who’s stronger Gold or the SPX.

May 19, 2024:

You can see Gold’s rally against the SPX starting at the 2000 low and how the 200 week sma usually does a good job of either holding support or resistance which ever side the ratio is trading.

March 11, 2024:

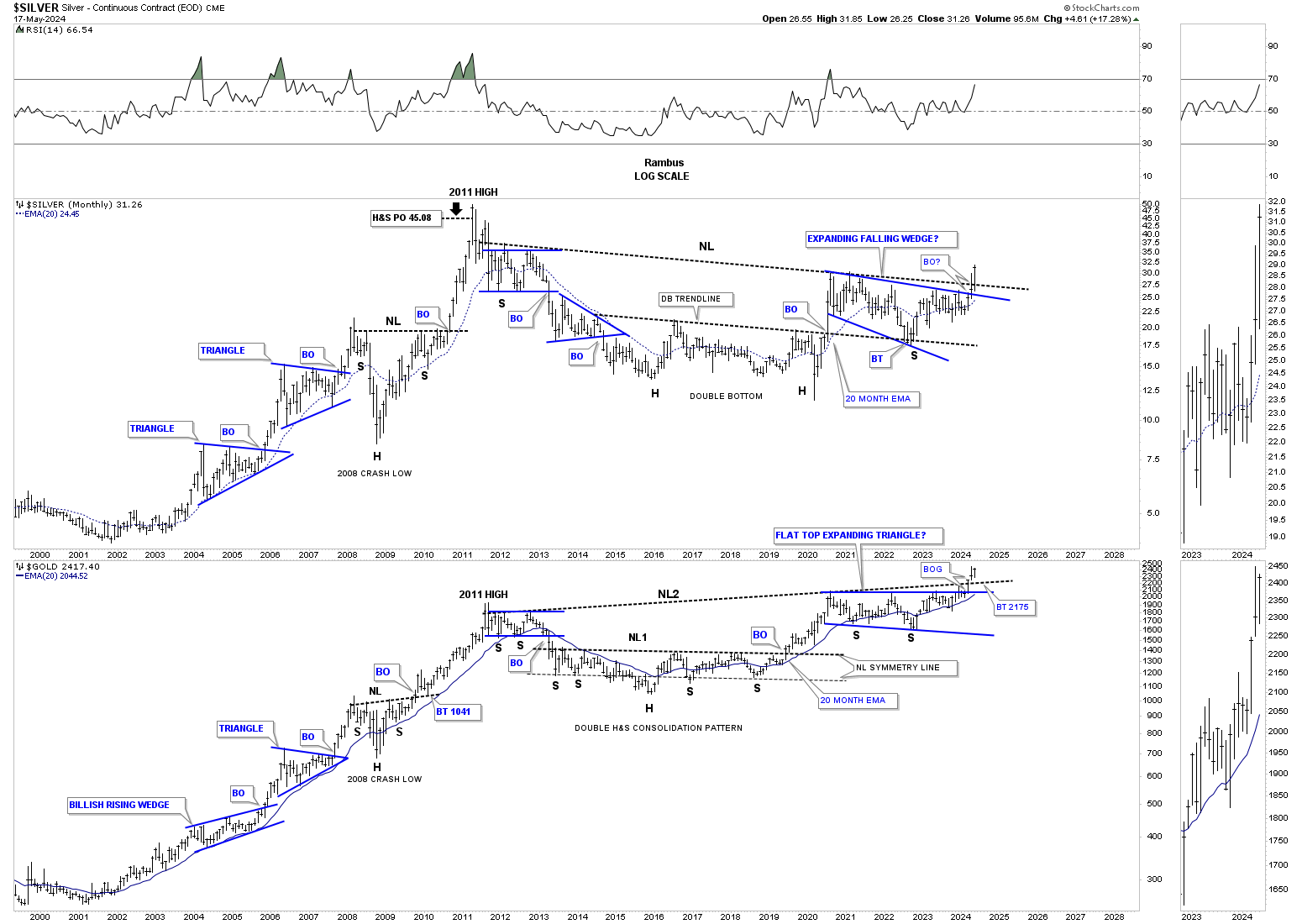

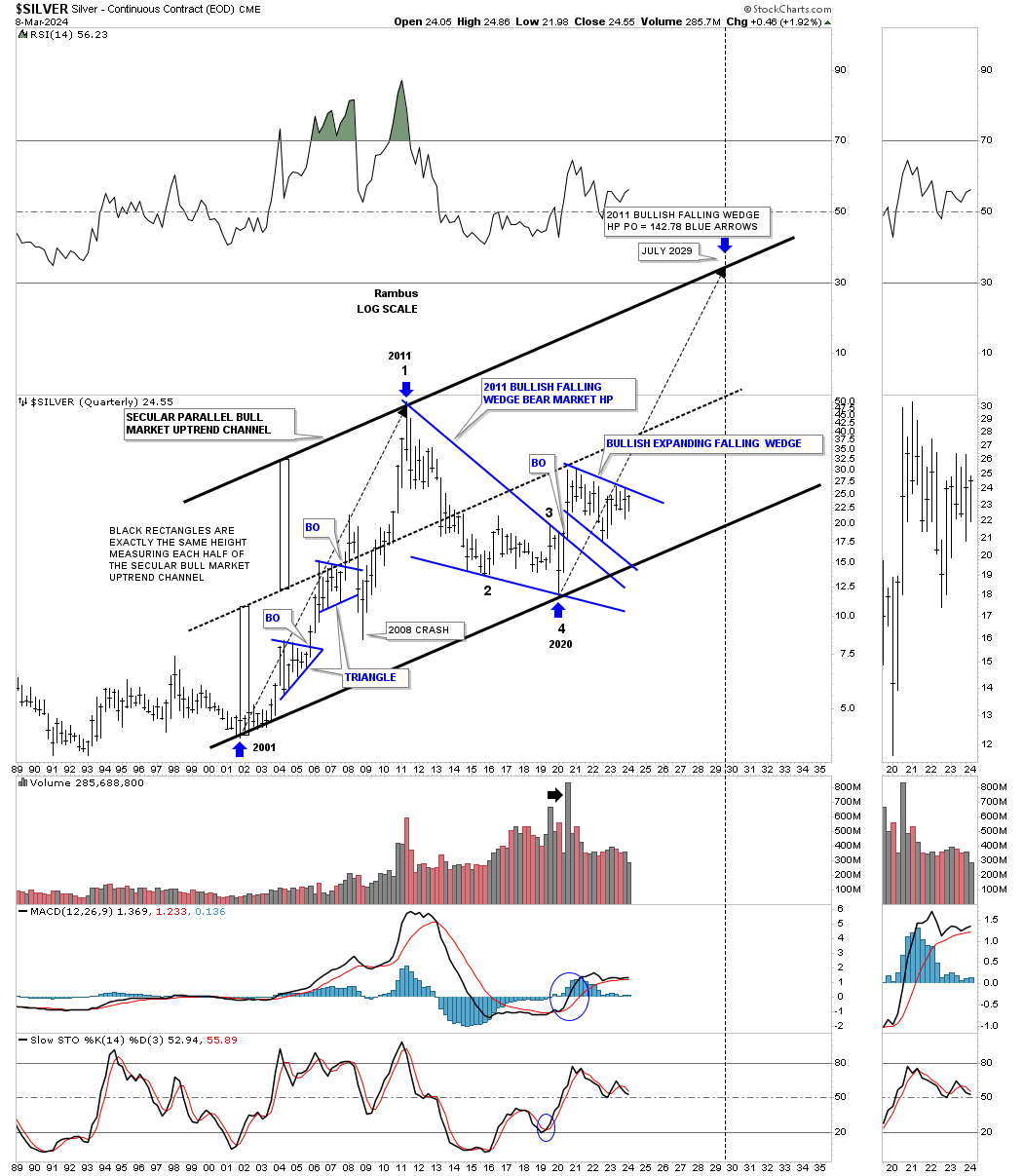

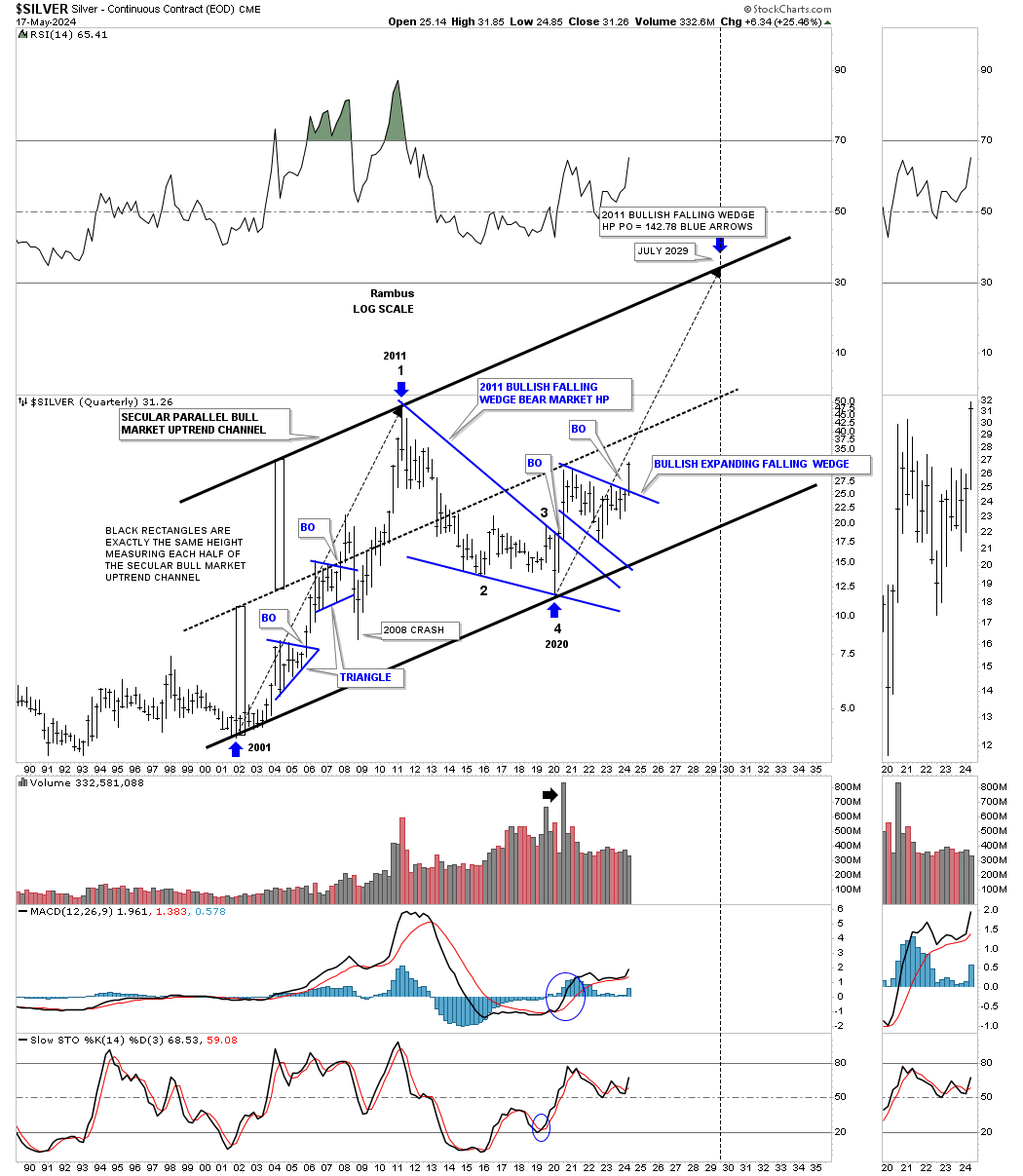

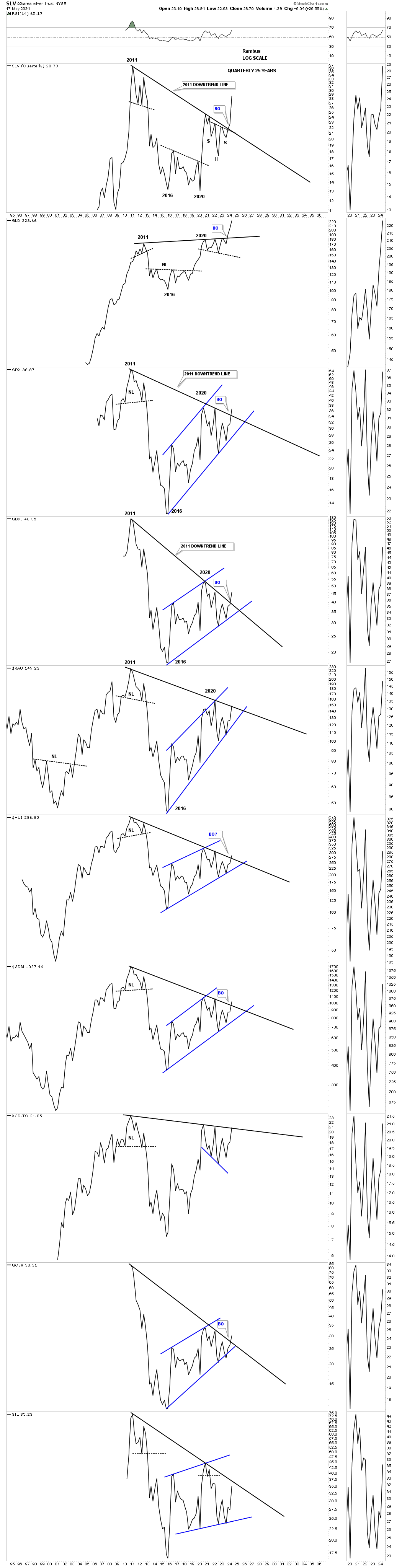

Lets take a quick look at Silver’s secular bull market which began a few years later than Gold’s. Unlike Gold which is trading at all time highs Silver is not even halfway back up to its all time high at 50. Its 2020 trading range shows the blue expanding falling wedge with the top trendline coming into focus once again after several previous touches.

The two long back arrows measure time and price. After topping out in April of 2011 Silver went on to form the 2011 falling wedge which I view will be a halfway pattern to the upside. The fractal nature of the markets suggests that the second leg up, which is now in progress since the last touch of the bottom trendline could be similar in nature to the first leg up into the 2011 all time high. The first big clue the secular bull markets is still alive and well would be to see the 2020 blue expanding falling wedge breakout to the upside.

May 19, 2024:

We got the very clean and large breakout. Clean because the price action opened above the top rail of the 2020 blue expanding falling wedge with no overlap.

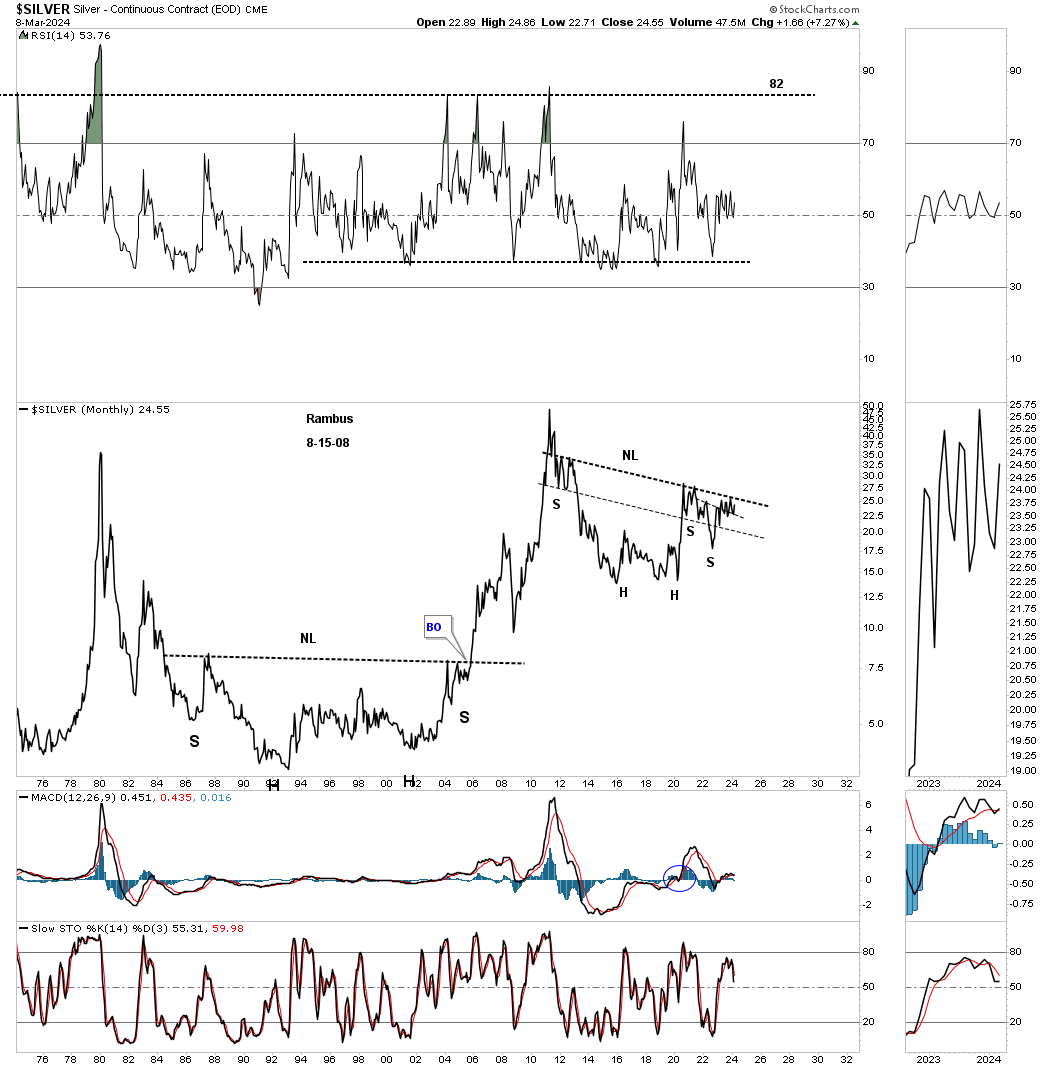

March 11, 2024:

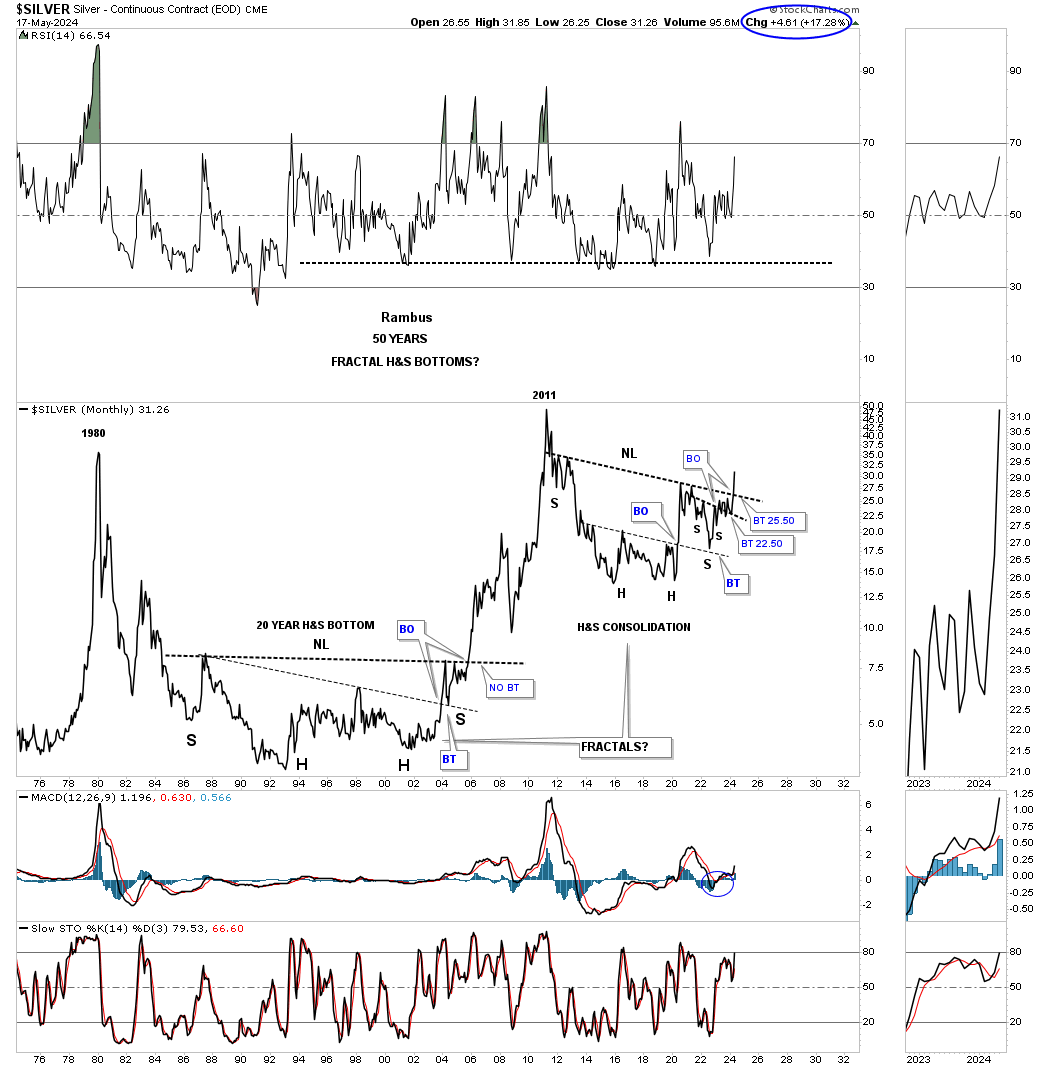

There is another pattern I’ve been following on Silver for several years which is the possible very large H&S consolidation pattern from the monthly line chart perspective. I’ve heard so many times through the years that you can’t trust a long term trading range and they are irrelevant. Note the massive H&S base that formed after the 1980 all time high that took nearly 20 years to complete before the neckline was finally taken out. Gold also formed a very similar 20 year base before its 1980 bear market came to an end in 2000.

May 19, 2024:

Again, we are only halfway through the 2nd quarter and Silver is showing a massive quarterly breakout.

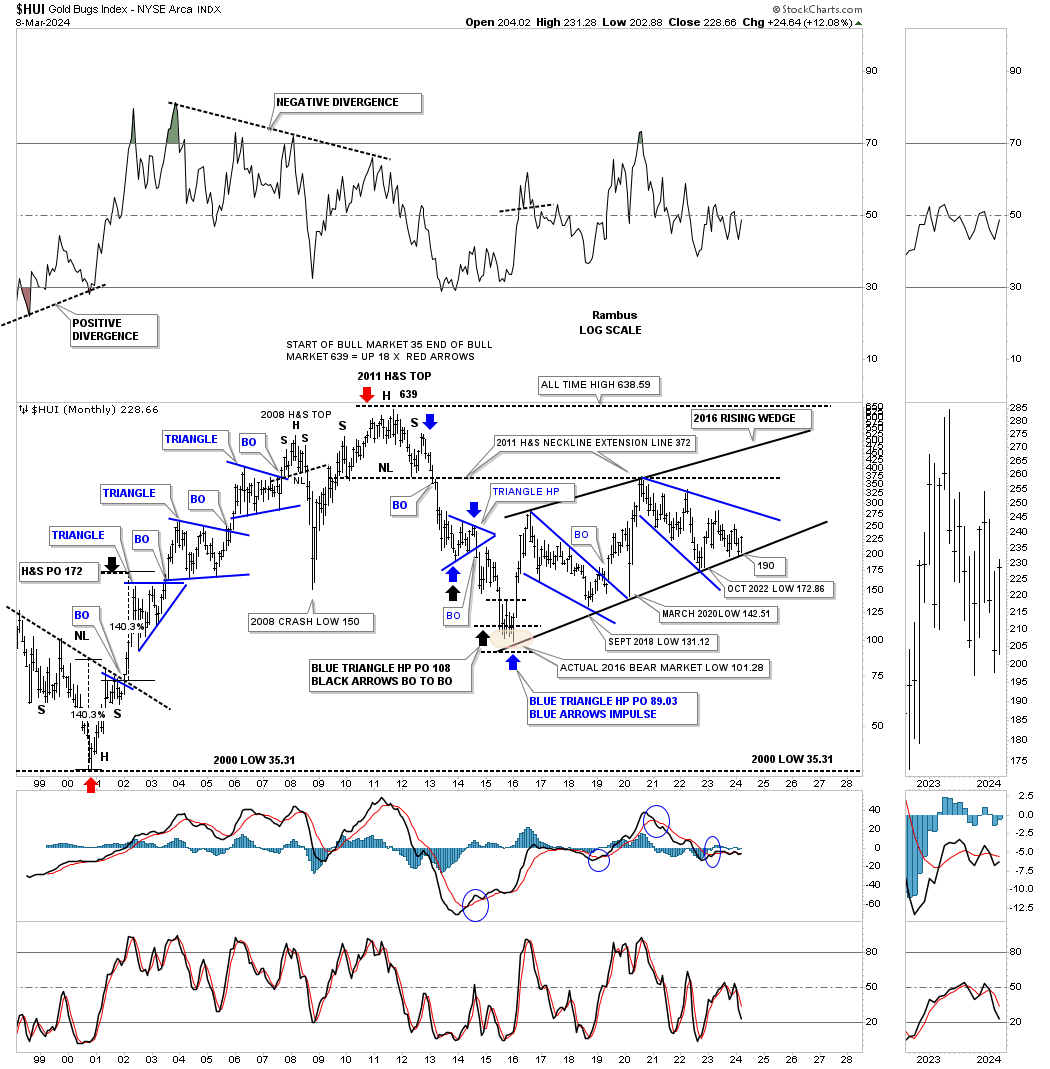

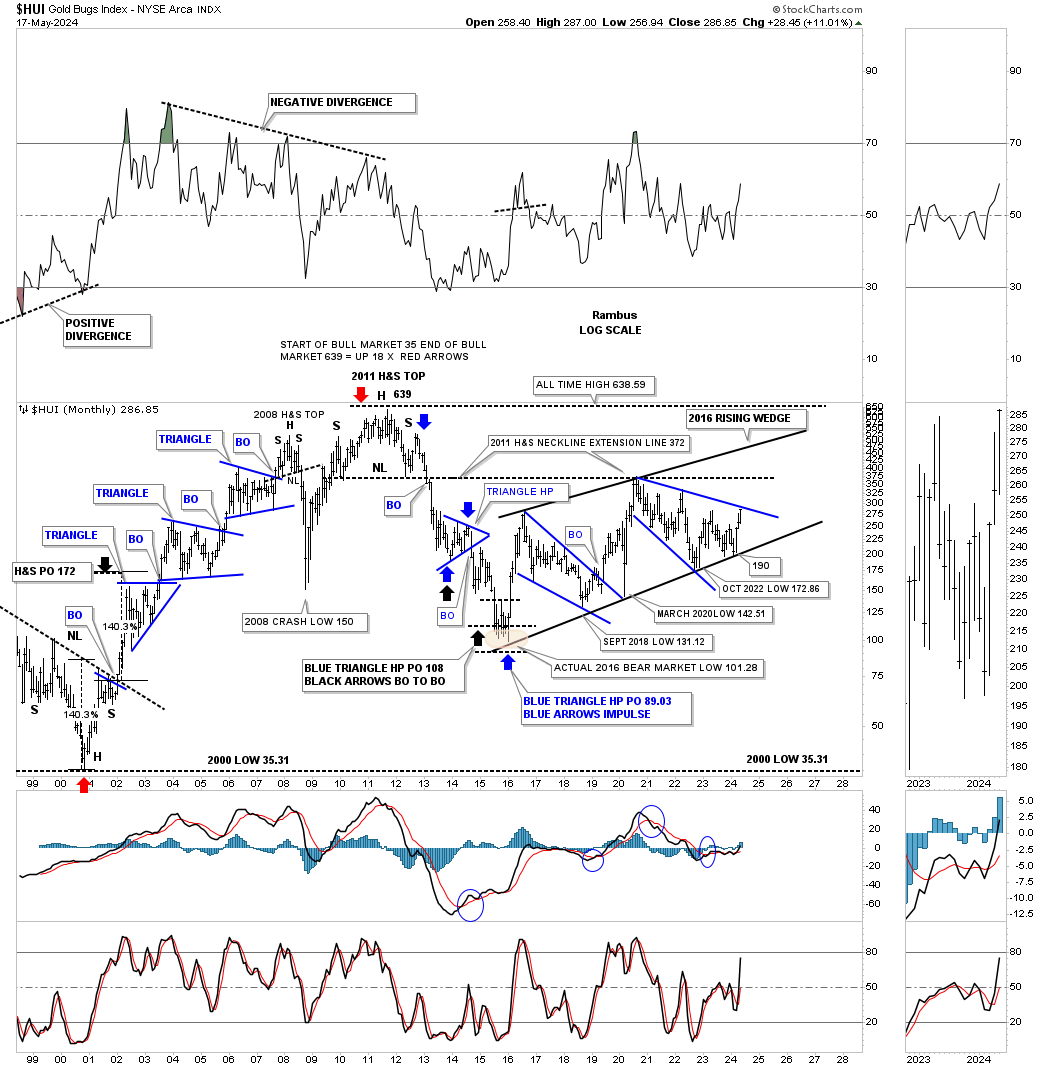

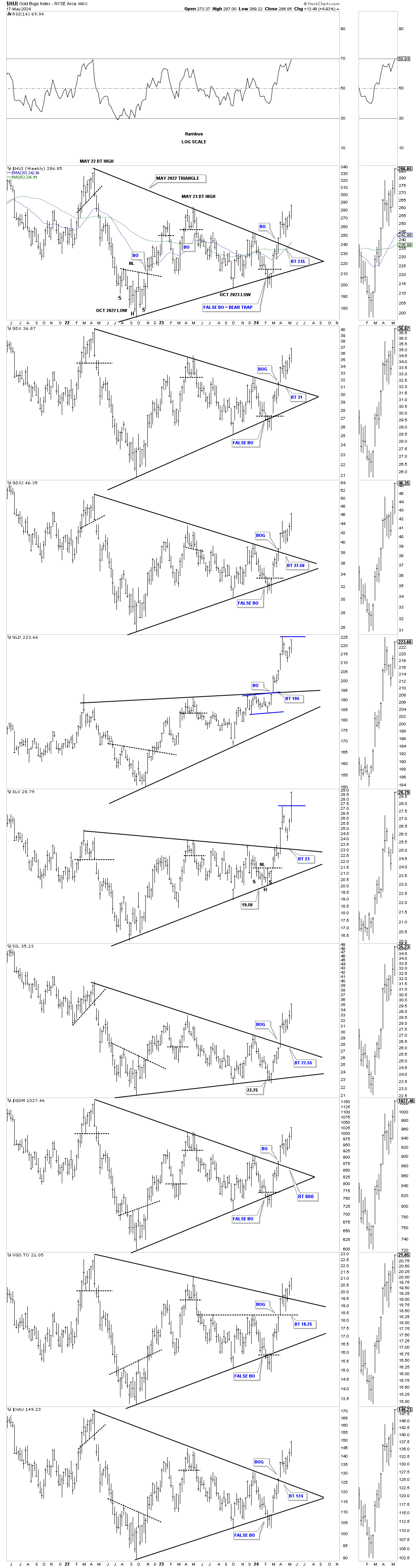

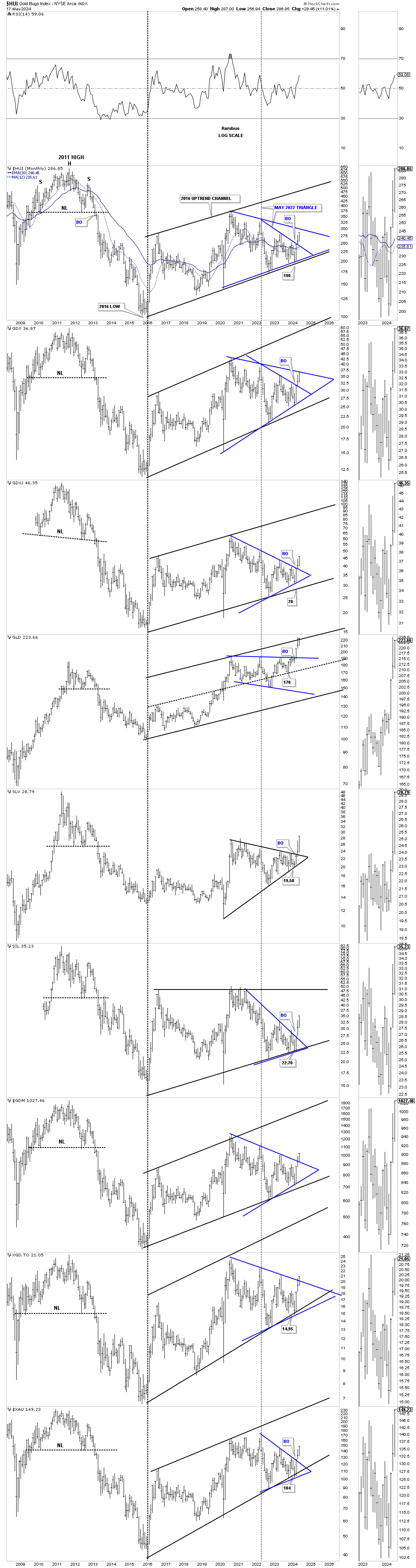

Lets take a quick look at the HUI which shows most of its history going back to the 2000 bear market low and the bull market that followed. Back then was the time to be invested in the PM stocks as one consolidation pattern formed on top of the previous one with a nice impulse move between each consolidation pattern. The HUI’s bull market came to an end when the head of the very symmetrical multi year H&S top formed in 2011.

Note the bottom trendline on the 2016 uptrend channel which has defined the bull market, if you can call it that, up to the present. It is an uptrend channel because the HUI has made higher highs and higher lows. Note that last monthly bar that just touched the bottom rail at the end of February with March showing us a nice rally right where we were hoping to see it.

March 11, 2024:

May 19, 2024:

The 2016 uptrend line held support and the HUI is now testing the top rail of its blue 2020 bullish expanding falling wedge.

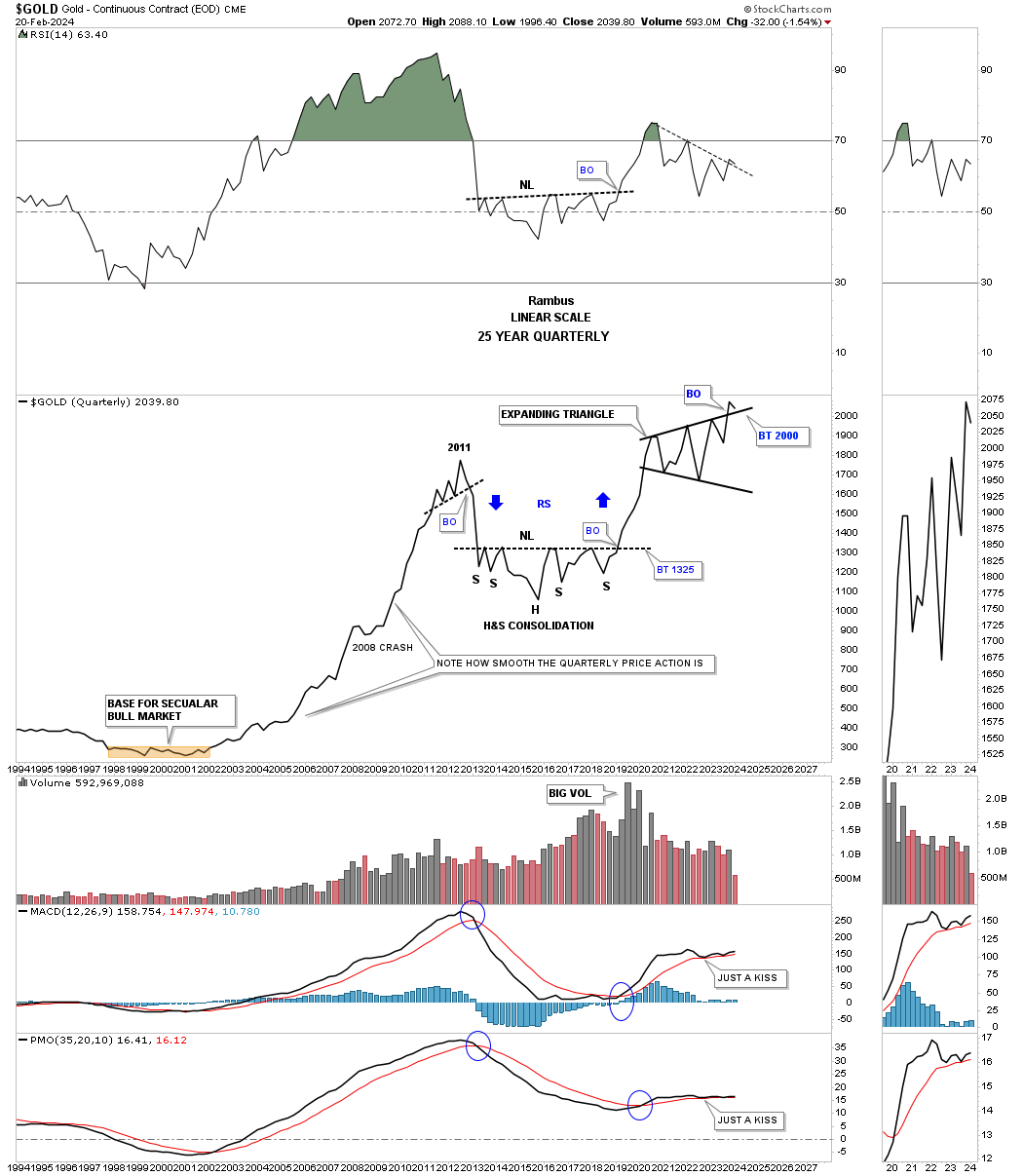

February 20, 2024:

There is a consolidation pattern I’ve been following on Gold which shows up on the quarterly line chart. For several years we’ve watch the price action touch the top tendline from below and fail to breakthrough. Back on February 20th I posted this chart in a Markets Update.

This is what I wrote on February 20th in regards the the 2020 black expanding triangle.

February 20th:

With less that six weeks left of trading for the 1st quarter of 2024 Gold has tested the top rail of the black expanding triangle. A bullish sign would be to see no backtest at the end of March, but a new higher high.

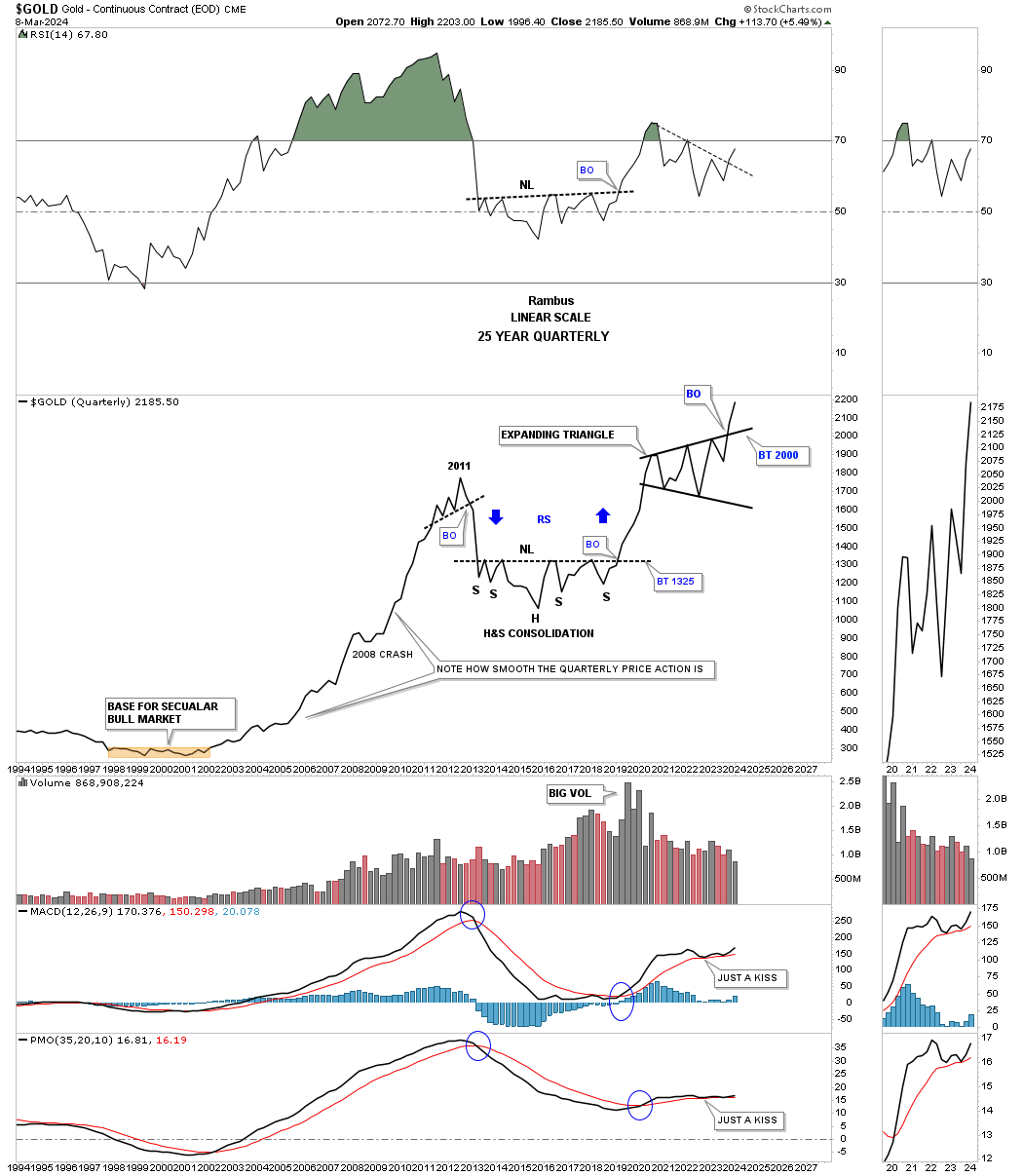

March 11, 2024:

When looking at Gold from the quarterly line chart perspective you don’t see many trading ranges and when you do you know they are important. Compare the exact same chart above to this one below. We still have three weeks of trading for March, but you can now see a higher high with the breakout looking more pronounced.

Also note from the quarterly line chart perspective how the bull and bear declines show almost a straight line. During the entire bull market from 2000 to the 2011 high you can see just a couple of modest one quarter declines with the biggest one being the 2008 crash low. Note how the reverse symmetry looked over the same area on the way down from the 2011 high to the first reversal point in the black expanding triangle as shown by the blue arrows.

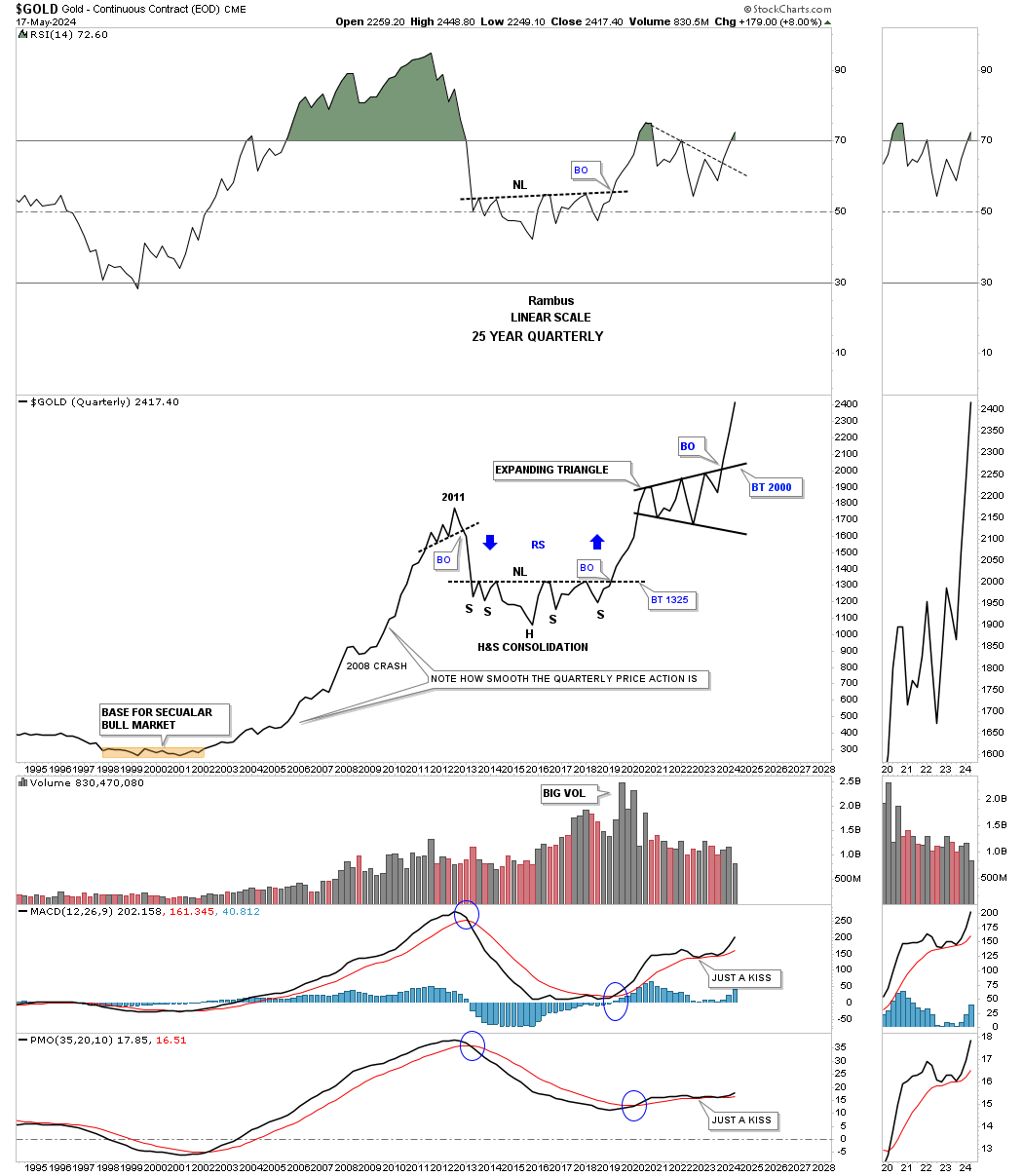

May 19, 2024:

The quarterly line is getting longer.

March 11, 2024:

We’ve looked at some long term charts tonight so lets look at one more I have been following for some time, but was waiting for the right time to post it. Through the years we’ve heard analyst calling for 10,000 gold or 20,000 gold which I thought were crazy price objectives.

If you go back up to where I posted the Gold:USD ratio which shows the 2011 triangle consolidation pattern that is the chart I got the idea for this possible scenario below which I know will sound ludicrous.

If we start at the 1980 all time high to the 20 year bear market low in 2000 you can see a nearly perfect 6 point bullish falling wedge. How do we know it is a 6 point bullish falling wedge, just look at the eleven year bull market that followed the breakout.

Just about every Gold analyst knows about the 2020 trading range with each giving the consolidation pattern their own name. I took it a step further and connected the 2011 high to the 2020 high to get the top trendline and then the two lows for the bottom trendline which shows a bullish rising wedge with the breakout taking place this month. Again, markets are fractal in nature so if the 2000 to 2011 bull market is one massive impulse move and the 2011 bullish rising wedge is the halfway pattern then we can measure the price objective that I like to use, impulse method, as shown by the blue arrows.

I’m not saying this is absolutely going to play out, but it is something that I can now watch to see how the second leg of the secular bull market tracks the first leg up into the 2011 high.

From a Chartology perspective I’m strongly suggesting that the next impulse move higher is now underway where there will be consolidation patterns that form along the way but they will be buying opportunities. As they say, we’ll know in the fullness of time. All the best…Rambus

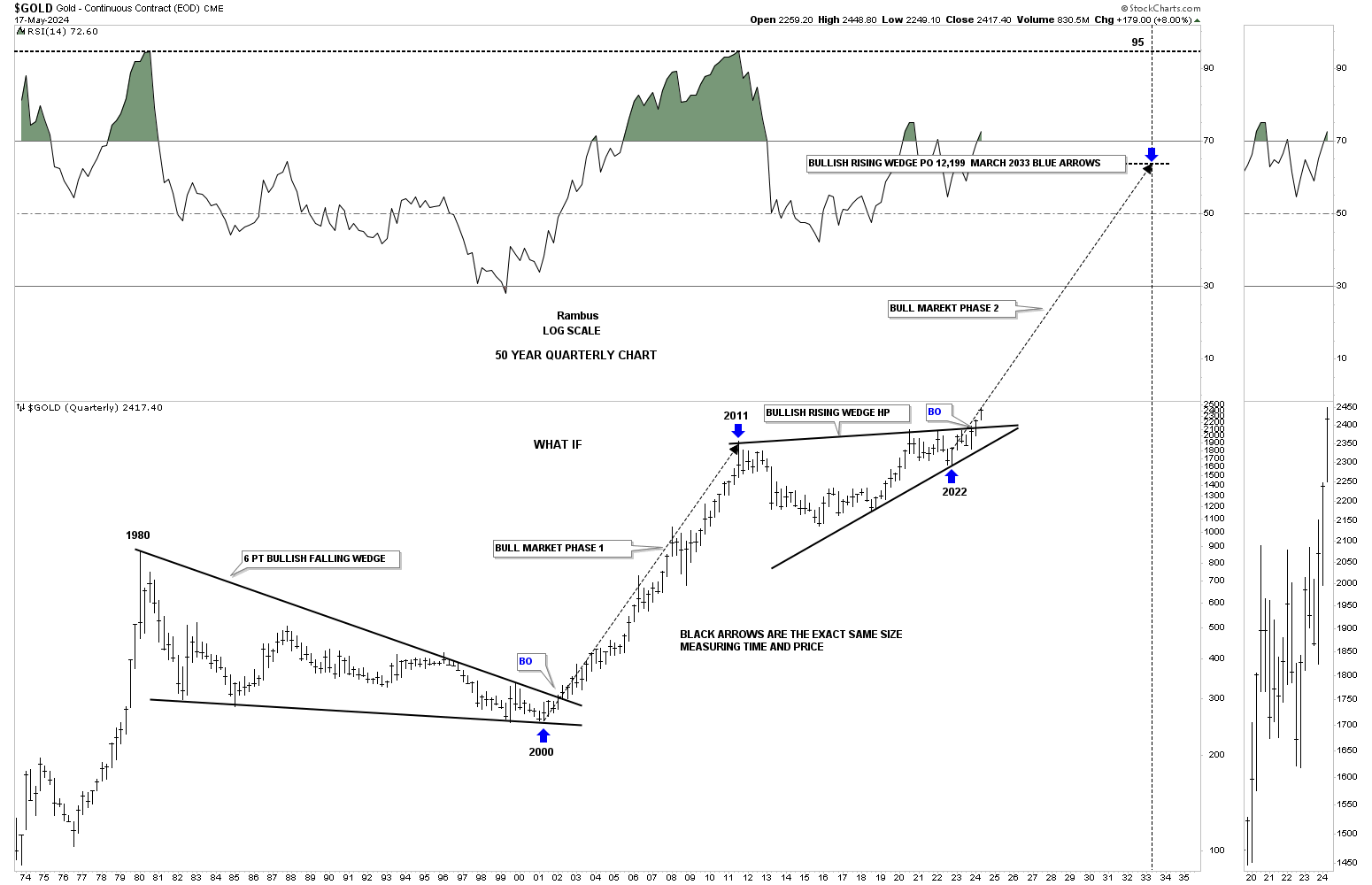

May 19, 2024:

We now have a 2nd quarterly bar forming above the top rail of the 2011 bullish rising wedge.

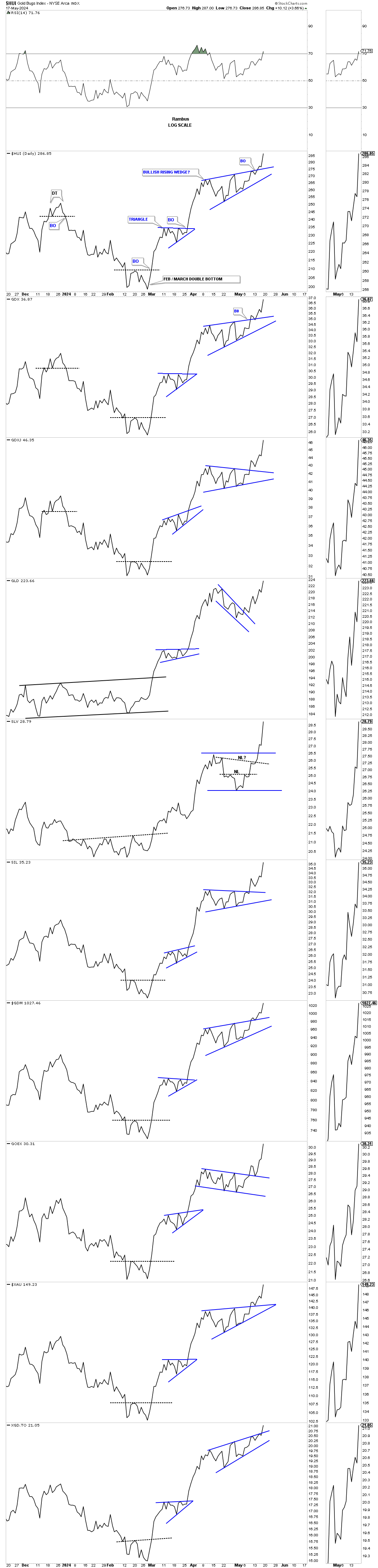

Since I didn’t update the charts last Friday that we’ve been following on the Markets Updates I’ll update some of them now.

This first chart is the daily line chart showing the February / March double bottom which launched this current leg of the bull market. Since the double bottom low I’ve been suggesting that in a very strong impulse move we should see up to three small consolidation patterns form before a much bigger one starts to build out to consolidate the big gains. Last week we saw the breakout from the 2nd small consolidation pattern, the blue bullish rising wedge which we know shows up in a strong impulse move.

Next is the weekly bar combo chart showing the May 2022 triangles with a nice clean breakout and no backtest at least so far. You can clearly see the false breakout below the bottom trendline in March which was negated when the price action traded back inside of the May 2022 triangle. That false breakout created a bear trap which usually leads to a strong move in the opposite direction and in this case up. We started the accumulation process for the PM Stock Trades Portfolio on the day of the close above the double bottom breakout on March 5th, March 4th for the first trades in the Kamikaze Portfolio.

Next is the long term monthly chart going back to the infamous 2011 very symmetrical H&S top which led to the bear market. The 2016 low ended the bear market where the price action has been trading in the 2016 uptrend channels in most cases with the May 2022 triangle forming the last third of the uptrend channel.

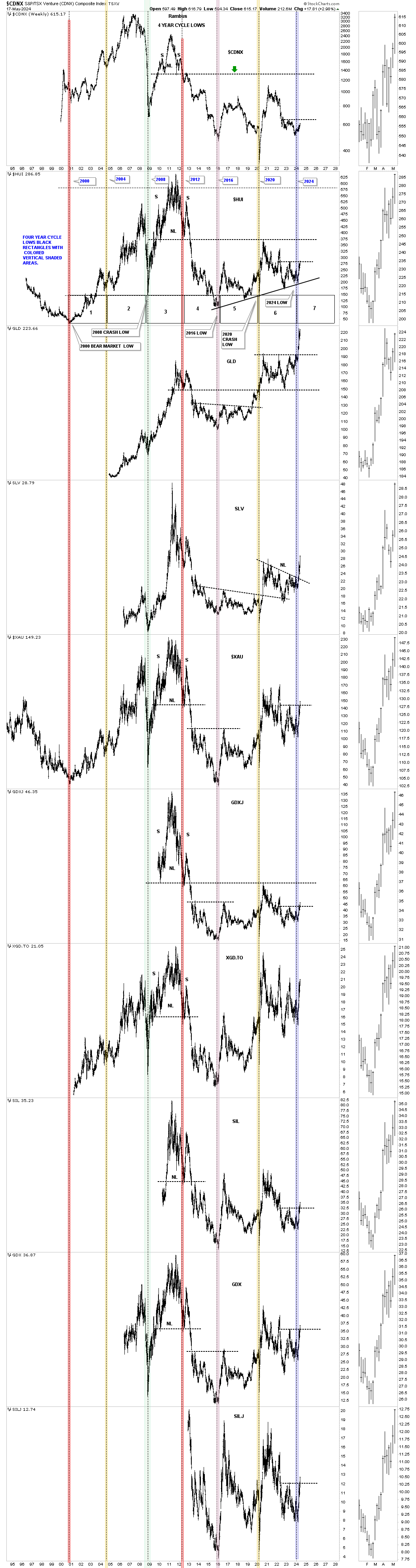

Next is the four year cycle low combo chart showing it nailed the recent four year cycle low.

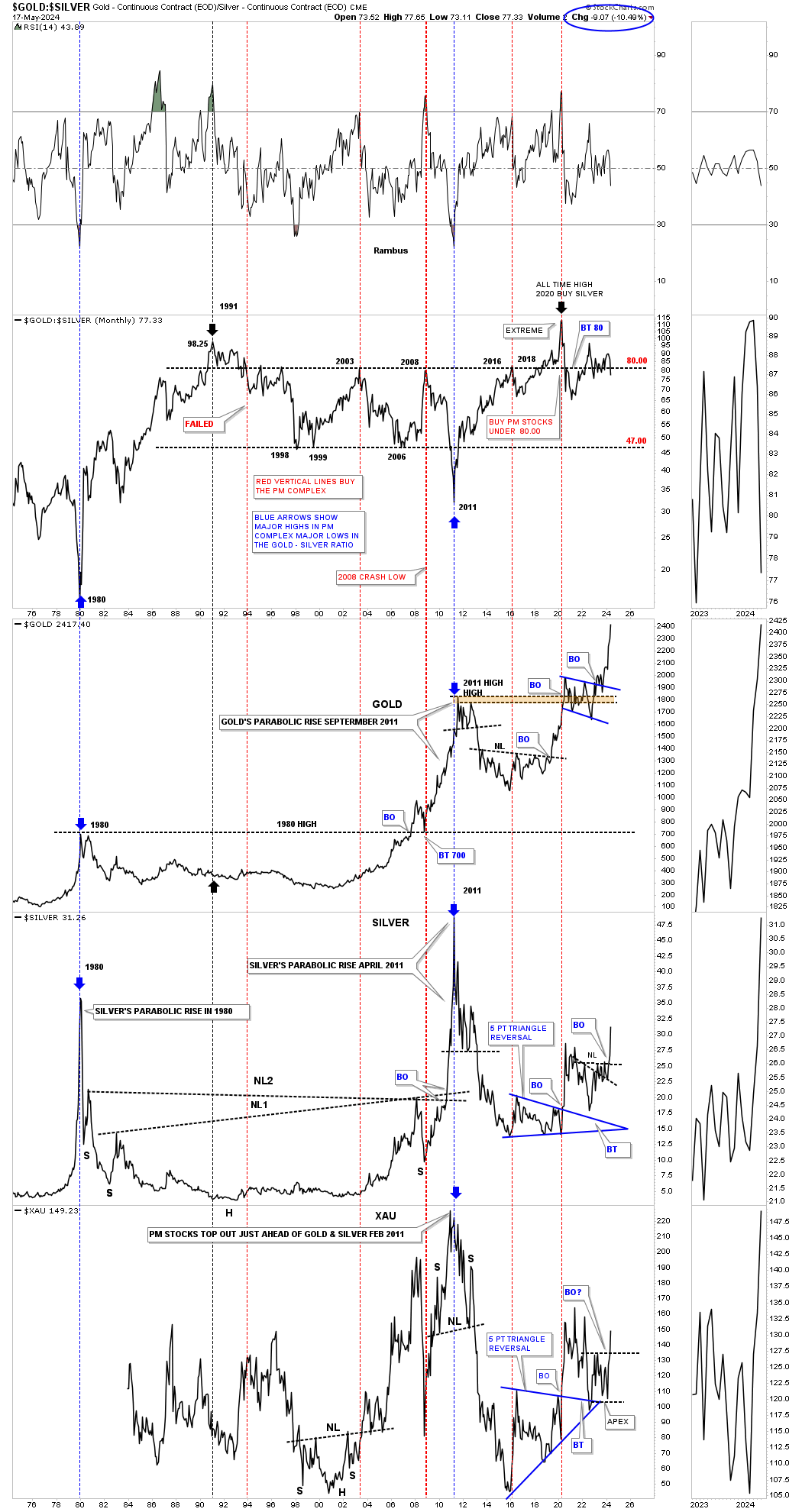

Another piece of the bullish puzzle finally happened when the Gold:Silve ratio just broke below 80 which can often times be a very bullish development for the entire PM complex.

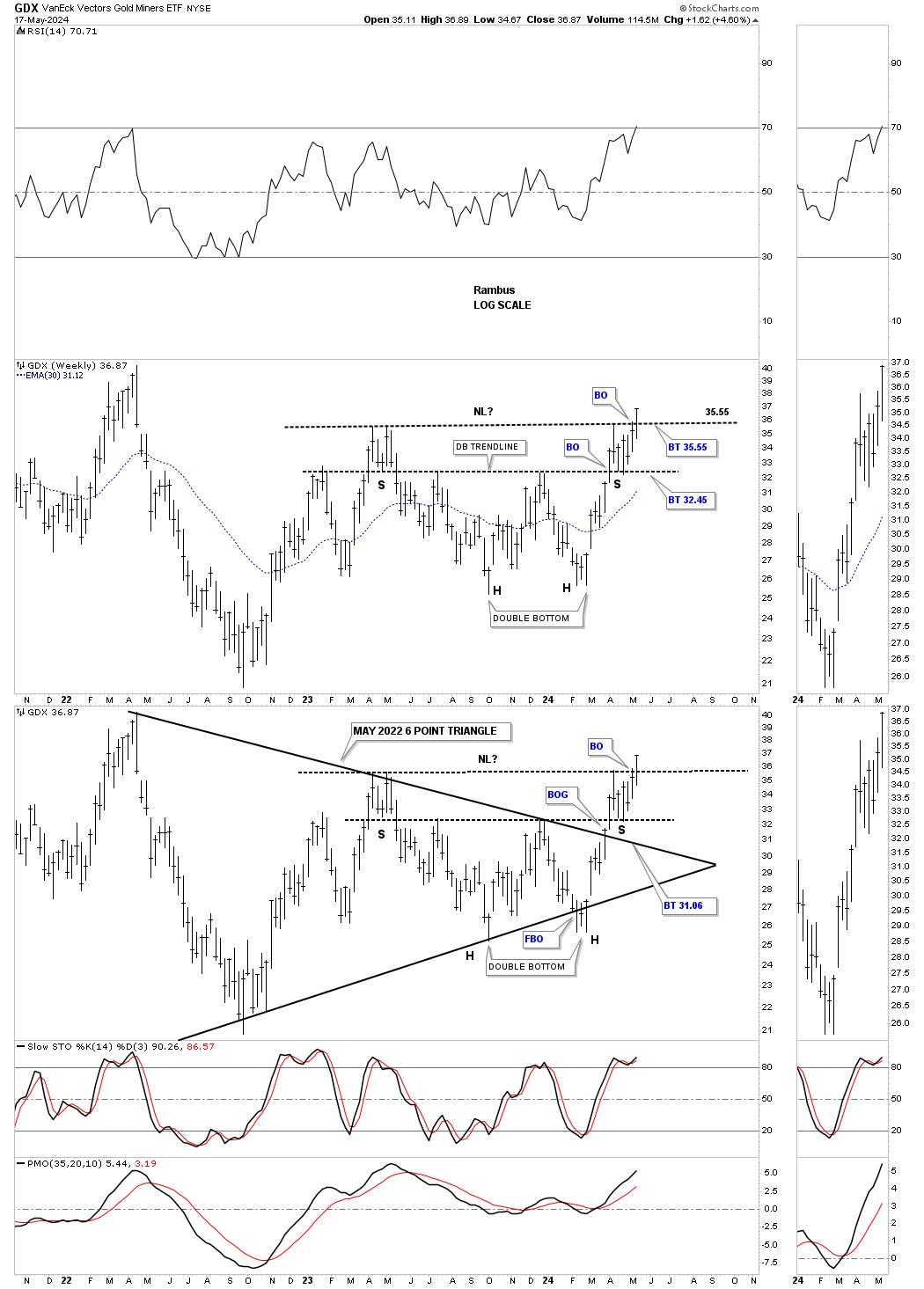

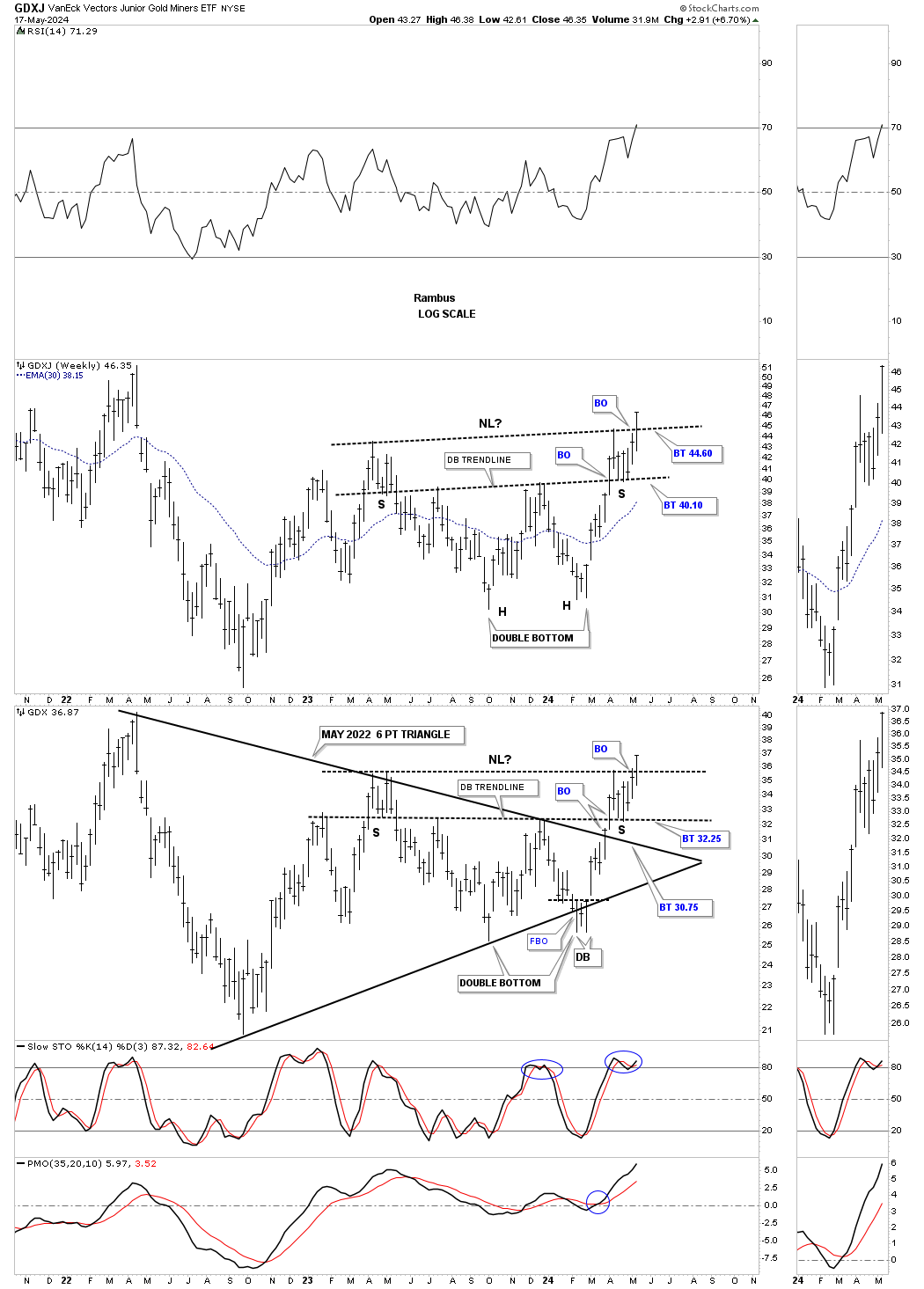

Next is the weekly combo chart for the GDX which shows the two shorter term patterns on a relative basis, the double headed H&S consolidation pattern on top with the May 2022 triangle below. I overlaid the double headed H&S consolidation pattern over the May 2022 triangle so you can see how the two very different patterns fit together. Last week we finally saw the breakout above the neckline which should now hold support on a backtest. Note the very nice symmetry between the left and right shoulders in time and price.

Same setup on the GDXJ.

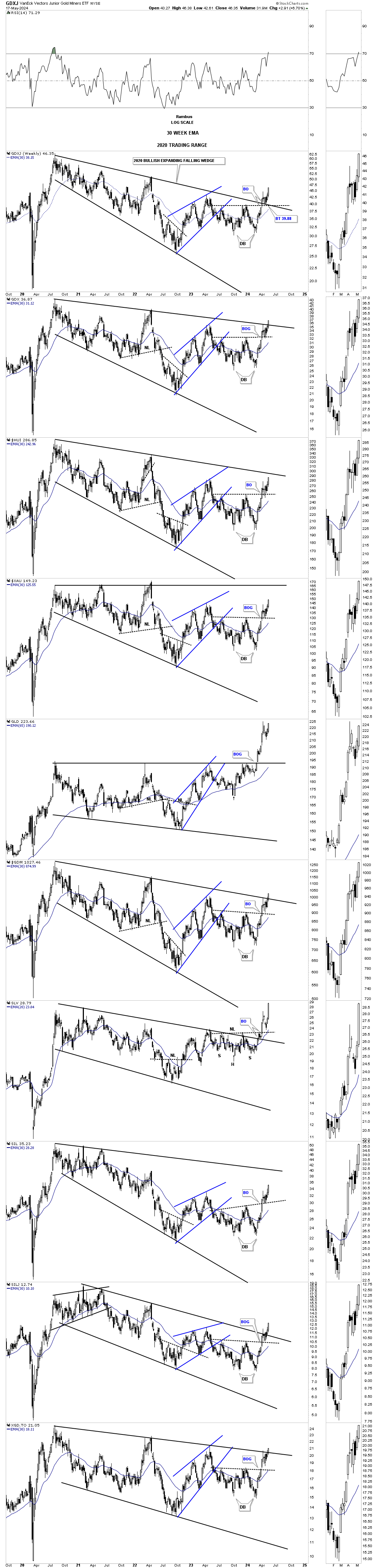

This weekly candlestick chart for the PM complex shows the large 2020 bullish expanding falling wedge from hell in most cases. For our long term members you know how long we’ve been following the formation wondering if we would ever see the breakout. Well the time has finally come with the GDXJ being the first PM stock index to breakout. As you can see there are others now that are in the process of breaking out.

From this weekly perspective you can see a double bottom with the left side being the October 2022 low and the right bottom being the October 2023 low with the micro March 2023 low being the very last reversal point.

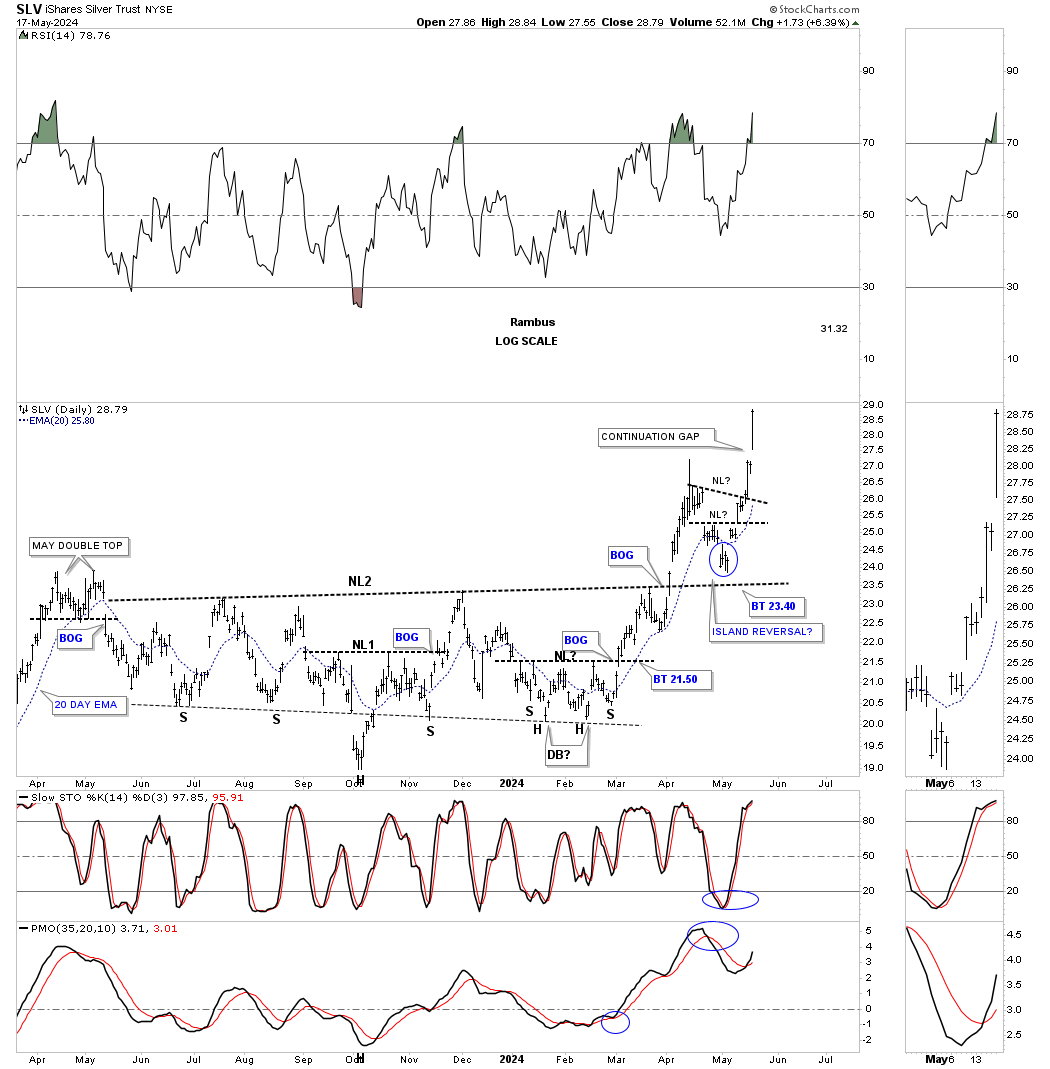

Silver was by far the winner last week with a move we haven’t seen in years. Below is the daily chart for SLV we’ve been following very closely which shows a H&S consolidation pattern with the much smaller H&S bottom forming the right shoulder low. After the initial breakout we saw that large daily reversal bar which suggested that part of the rally was most likely over. We then got a backtest to the neckline which came up just a bit short when the island reversal pattern formed reversing the move from down to up. There is a good chance that last Fridays monster move, which opened with a gap, has more room to run before its time to consolidate. Friday’s gap looks like it could be a continuation gap or a halfway gap to the upside.

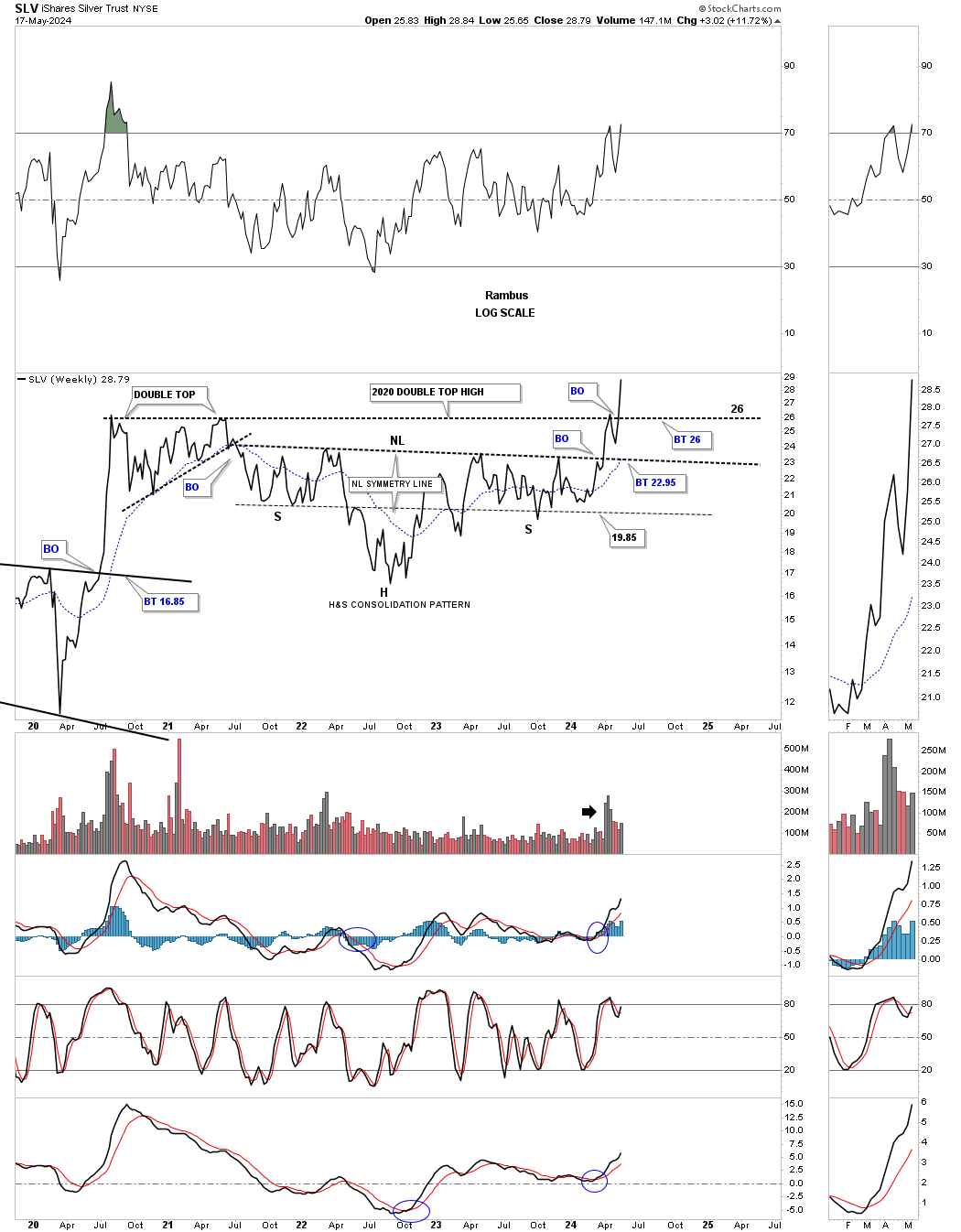

Next is the weekly line chart for SLV showing its large H&S consolidation pattern with the right shoulder being the smaller H&S consolidation pattern on the daily chart above. I’ve been mentioning how the 2022 double top was going to offer initial resistance and that it could take a few hits before the resistance finally gives way to the bulls. Friday’s price action put the final nail in the coffin for the bears hoping the 2022 double top high would hold. We could still see a backtest, but if the continuation gap on the daily chart above is any indication we most likely won’t see a backtest.

This next long term quarterly line chart shows the 2011 downtrend line we’ve been following for a long time. Gold was by far the first to break that 2011 bear market downtrend line with Silver breaking it just recently. Now many more of the PM stock indexes are taking their turn to breakout adding another very important piece to the puzzle.

I know this has been a long post, but after 4 1/2 years of waiting, we just needed to put some of the big pieces of the puzzle we’ve been working on in place to gain perspective of where we’ve been and where we are going.

Again, for longer term members that remember when I first posted this combo chart for Silver and Gold did you really think these massive H&S consolidation patterns had a chance? You know what they say, Big Chart Patterns Lead to Big Moves. All the best. Rambus